The Open Network (TON): an institutional research note

![]() 32 Min. Lesezeit

32 Min. Lesezeit

- Ethereum

- Altcoins

Data as of 11th May 2026.

Summary

TON has solved distribution better than any Layer 1 to date but has not yet proven monetisation, retention or token-level value capture. The 12-month investment case rests on whether that gap closes.

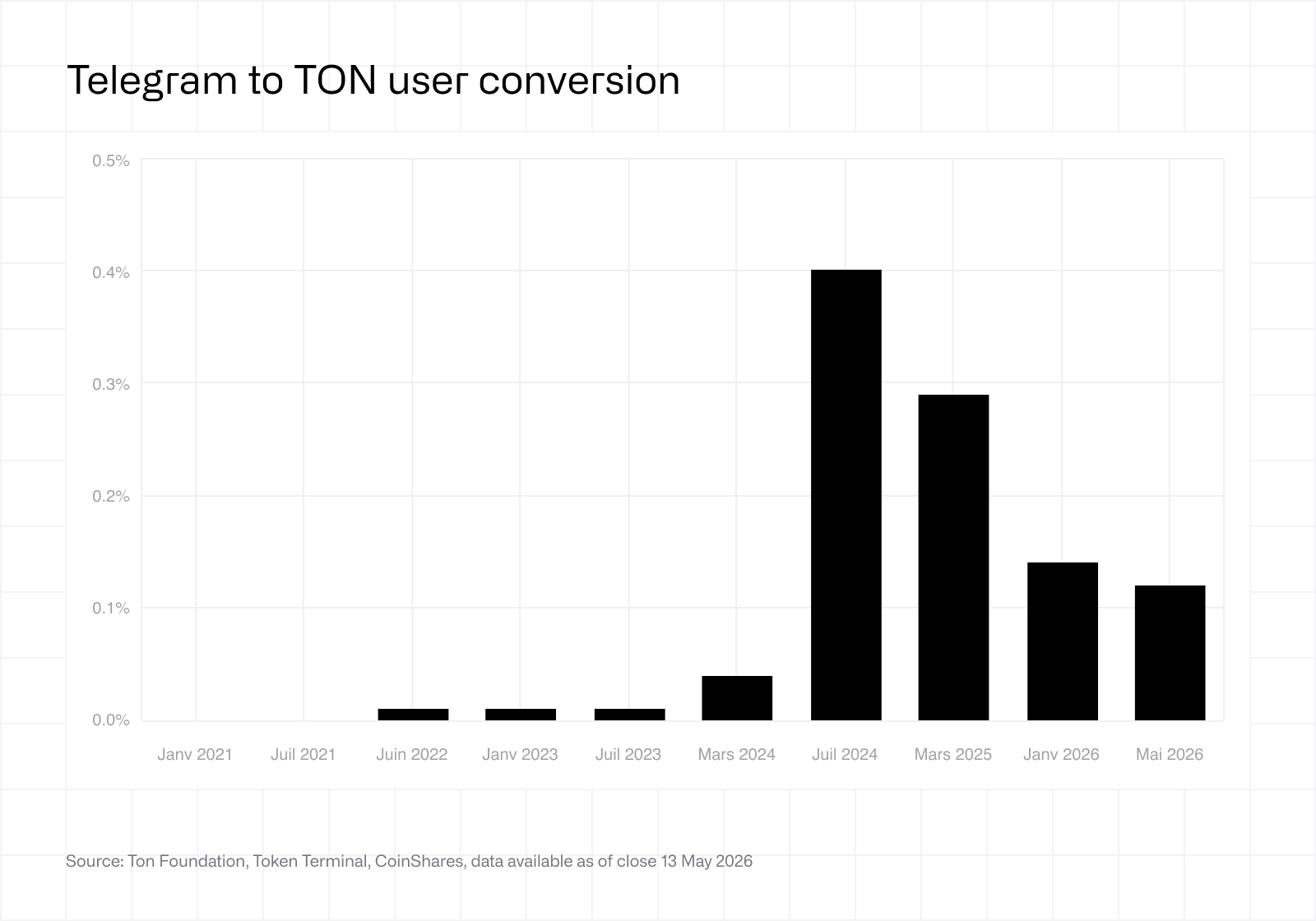

The central institutional question is whether on-chain economic activity, currently a small fraction of Telegram's headline reach, converges with the distribution. Telegram's 1 billion monthly active users compares with approximately 1.78 million monthly active TON wallets, a conversion ratio of 0.12% on the latest data.

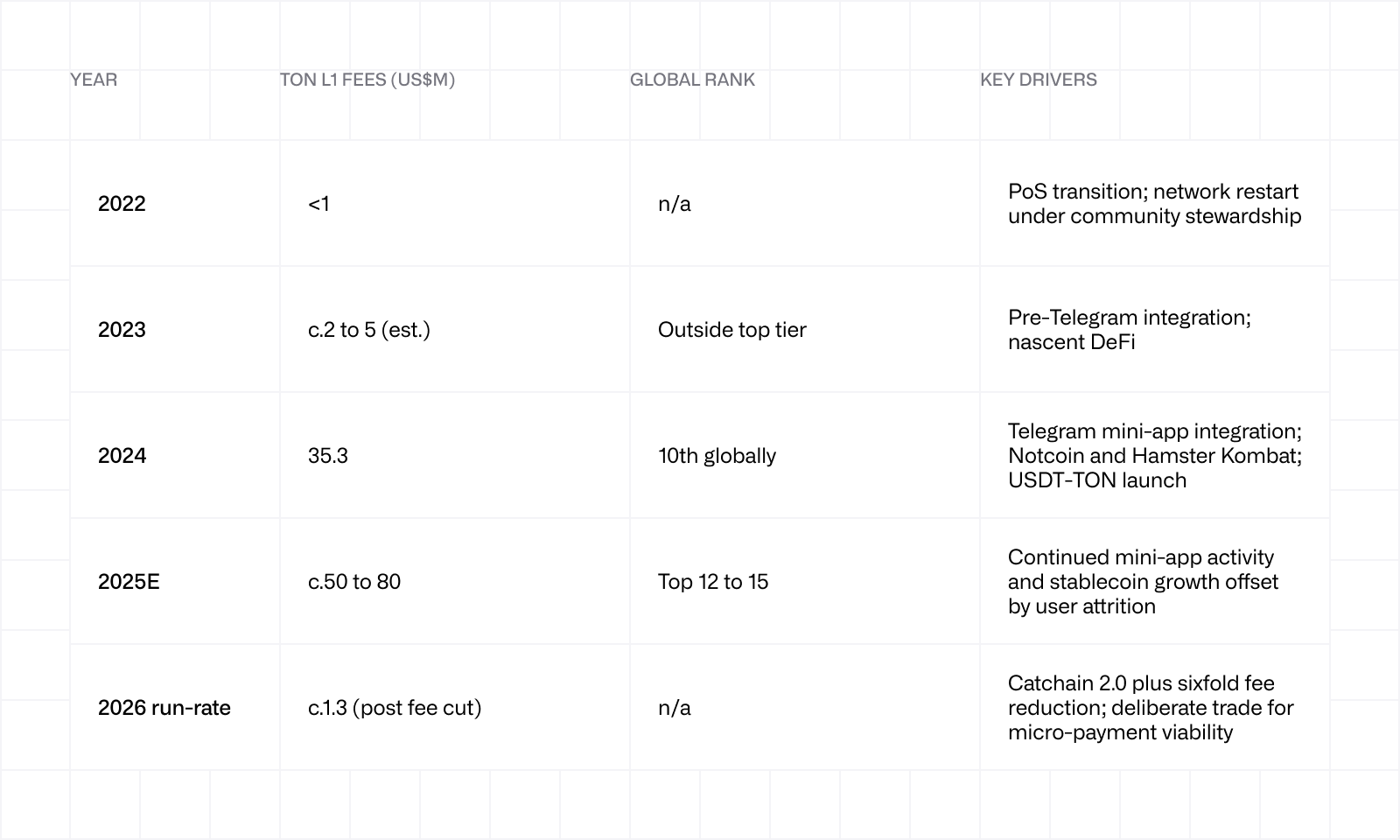

Network fee earnings rose from a negligible base in 2023 to US$35.3M in 2024 (10th globally), before stepping down sharply in early 2026 to roughly US$1.3M annualised following a deliberate sixfold fee cut intended to enable micro-transaction use cases.

The April 2026 Catchain 2.0 consensus upgrade cut block times from roughly 2.5 seconds to 400 milliseconds, raised throughput tenfold, and reduced finality to approximately 1 second.

Telegram's direct operational control of TON, announced on 4th May 2026, removes governance ambiguity but tightens single-platform dependency.

Post-Catchain 2.0, network gross staking yield jumped to 16.7% annualised from approximately 4% pre-upgrade. TON now offers the highest staking APR among the top 50 cryptocurrencies. Adjusted for through-2028 unlock dilution, real economic carry is materially lower than the headline figure.

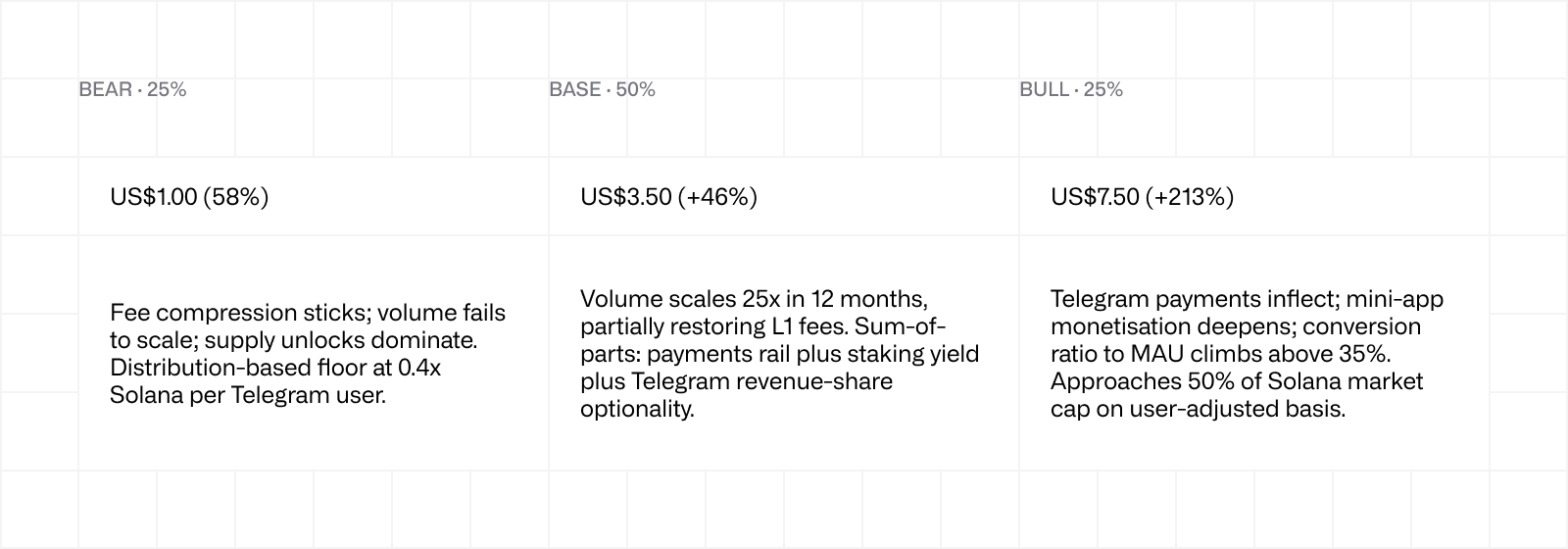

Base case 12-month price of US$3.50 (+46% vs spot of US$2.40), bear US$1.00, bull US$7.50.

Principal risks: the rolling unlock of approximately 37 million GRAM (formerly TON) every 30 days through to April 2029, the 1,081M GRAM whale freeze release on 21st February 2027, single-platform dependency, validator concentration, and the now-deliberate compression of L1 fee revenue.

1. Network architecture

The Open Network is a Layer 1 proof-of-stake blockchain originally developed by Telegram's founders in 2018 and relaunched under the TON Foundation after Telegram's 2020 exit. Architecture rests on what TON calls the Infinite Sharding Paradigm, in which the network dynamically splits into up to 2^60 shardchains coordinated by a central masterchain. In practice the design is intended to allow throughput to scale with demand rather than against a fixed block-space ceiling.

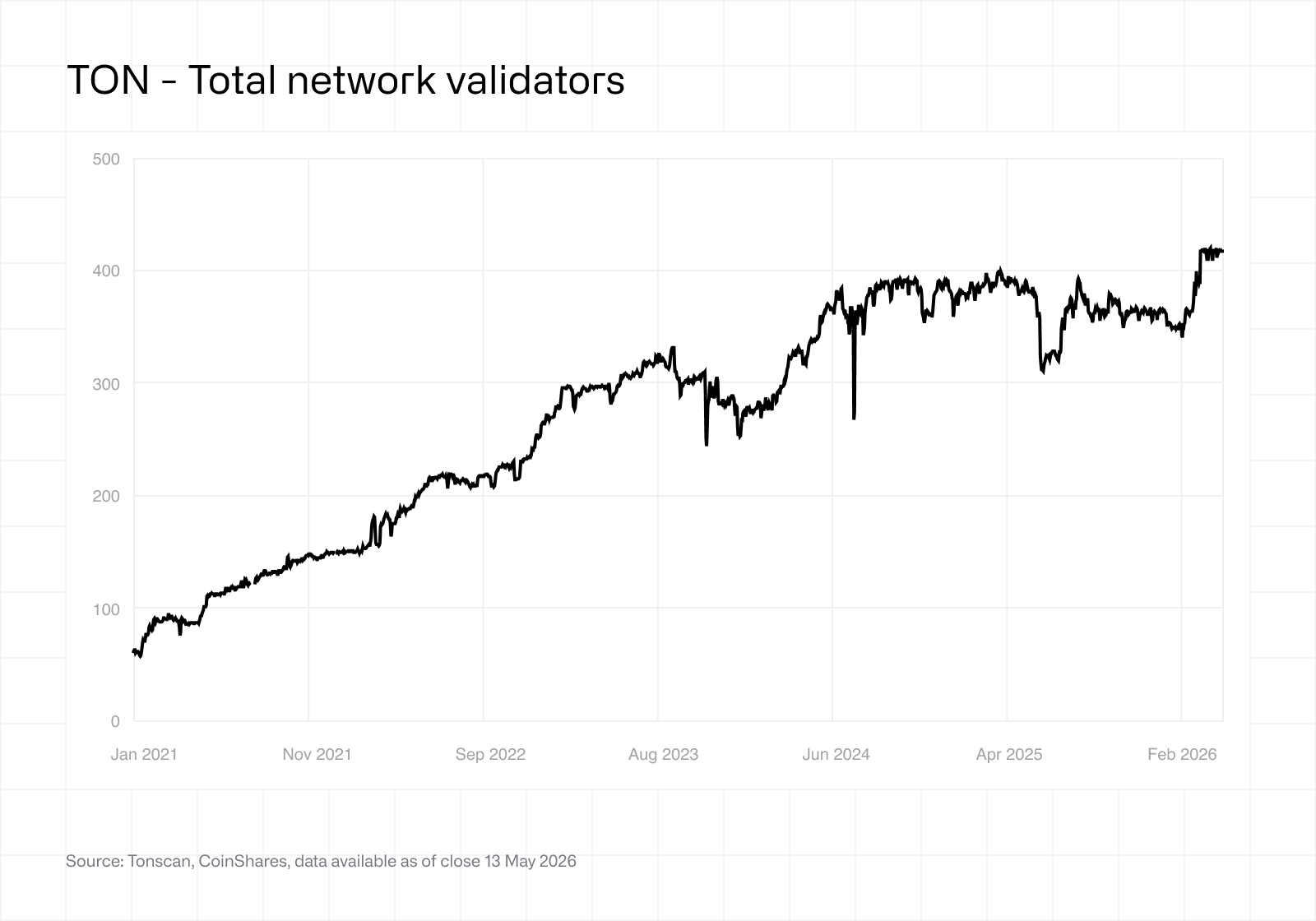

The native token, GRAM (formerly Toncoin), is used to pay transaction fees, secure the network through staking, and act as the medium of exchange within the TON Wallet integrated into Telegram. Around 421 active validators currently secure the network, with a typical minimum effective stake of approximately 1 million GRAM. Half of transaction fees are burned and the remainder distributed to validators, alongside a base block subsidy of 1.7 GRAM per masterchain block and 1 GRAM per basechain block.

2. Recent upgrades

Four technical and governance changes over the past two months have reshaped the network materially.

Catchain 2.0 activated on 9th April 2026, reducing block production from roughly 2.5 seconds to 400 milliseconds and increasing estimated throughput by approximately 10x. Transaction finality fell from around 10 seconds to roughly 1 second, with some measurements as low as 600 milliseconds. The upgrade brings TON's performance envelope closer to Solana's claimed transaction-per-second capability, though TON's empirical daily throughput of around 2.16 million transactions remains well below Solana's roughly 72 million.

Fee reduction. On 1st May 2026 base transaction costs were cut by approximately sixfold to around 0.00039 GRAM, or roughly US$0.0005. The economic intent is to make micro-payments and per-action settlement viable inside Telegram applications, where pricing must approach zero for mass-market adoption.

Telegram operational control. On 4th May 2026 Pavel Durov announced that Telegram would take over the TON Foundation's principal operating responsibilities and become the network's largest validator, staking approximately 2.2 million GRAM. This consolidates governance and removes the prior arms-length structure. The market reaction was sharply positive, with GRAM rising roughly 79% in the seven days to 11th May 2026 and trading at approximately US$2.40 on a circulating market capitalisation of US$6.5B.Rebranding. On 1st June 2026, Pavel Durov announced that Toncoin would be renamed Gram, the original name used in the first whitepaper. The new name was validated by a community vote on 8th June 2026. TON remains the name of the network.

Further roadmap items include the TON Teleport trustless Bitcoin bridge (mid-2026), AppKit and AgenticKit developer toolchains, and a Rust node implementation.

3. User base and on-chain metrics

The headline distribution numbers are the strongest part of the TON case. Telegram crossed 1 billion monthly active users (MAU) in March 2025, alongside approximately 500 million daily active users. By early 2026 over 100 million users were managing digital assets through the Telegram-integrated TON Wallet, and cumulative on-chain account activations reached approximately 162 million.

On-chain activity has not scaled in step. Recent data indicate:

Daily transactions: approximately 2.16 million

Weekly active transactions: approximately 3.8 million (+32% week on week)

Monthly active wallets: approximately 1.78 million

Daily new wallet activations: approximately 43,600

The ratio of monthly active wallets to Telegram monthly actives is 0.12% on the latest data, which is the central data point of the investment debate. Distribution is unprecedented; conversion to economically active on-chain use remains low.

The 1B MAU figure is the unrestricted-access ceiling rather than the realisable monetisable footprint. Adjusted for fully blocked jurisdictions (China, Iran, Pakistan, Saudi Arabia and others), and the substantial share of users who will not interact with wallets, stablecoins or mini-apps regardless of UX improvements, the addressable base for on-chain conversion is materially smaller. We use the 1B figure as a denominator for comparability with other platform metrics, but our valuation framework treats the 0.12% conversion ratio as the binding variable rather than the absolute reach number.

The 1B MAU figure is the unrestricted-access ceiling rather than the realisable monetisable footprint. Adjusted for fully blocked jurisdictions (China, Iran, Pakistan, Saudi Arabia and others), and the substantial share of users who will not interact with wallets, stablecoins or mini-apps regardless of UX improvements, the addressable base for on-chain conversion is materially smaller. We use the 1B figure as a denominator for comparability with other platform metrics, but our valuation framework treats the 0.12% conversion ratio as the binding variable rather than the absolute reach number.

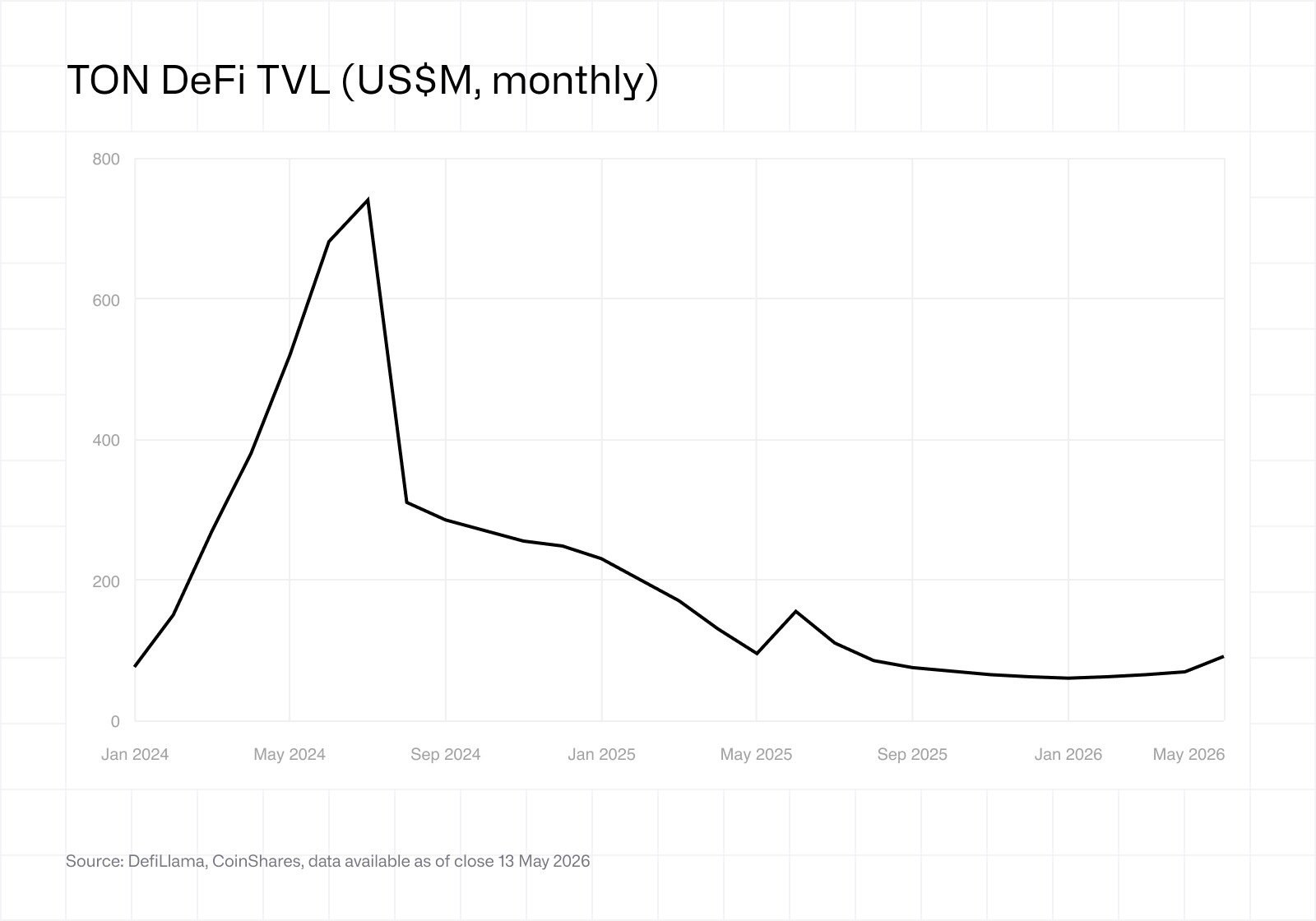

DeFi metrics underline the gap. TON's total value locked stood at approximately US$91.0M on 8th May 2026, up sharply from US$59.0M a few days earlier but well below the July 2024 peak of approximately US$740M. Weekly DEX volume recently approached US$42.0M. By contrast, Ethereum holds US$45.5B in TVL (a 53% share of global DeFi) and Solana around 6.8%, highlighting that TON is still in its infancy on this metric.

Stablecoin presence is more constructive: USDT on TON expanded rapidly following its May 2024 launch, anchoring stablecoin liquidity above US$750M, with cross-border payment use cases inside Telegram emerging as the most plausible non-speculative demand driver.

Stablecoin presence is more constructive: USDT on TON expanded rapidly following its May 2024 launch, anchoring stablecoin liquidity above US$750M, with cross-border payment use cases inside Telegram emerging as the most plausible non-speculative demand driver.

4. Tokenomics

GRAM (formerly Toncoin) has an inflationary supply curve, with current net inflation reported in the low single digits and as low as 0.6% on certain dashboards after fee burn is netted off. Validator emissions consist of the base block subsidy plus a share of fees. Approximately 1.2 billion GRAM, or around 9% of total supply, is staked.

Headline staking yields stepped up materially following the April 2026 Catchain 2.0 upgrade. Network-wide gross staking yield rose to 1.39% in April 2026 from 0.34% in March 2026, an approximately fourfold month-on-month increase translating to approximately 16.7% annualised. TON now offers the highest staking APR among the top 50 cryptocurrencies. The upgrade increased validator block subsidy throughput and shifted consensus economics in favour of stakers. The 16.7% gross figure is verifiable on the TON Foundation Dune dashboard (dune.com/ton_foundation/staking) and was confirmed in TON Strategy Company's Q1 2026 earnings (12th May 2026). Net institutional yield after pool commissions runs at approximately 14% to 16%, and this is now the relevant benchmark for institutional allocators modelling staking income.

The 14% to 16% net headline yield is a nominal figure, not a risk- or dilution-adjusted carry. Through to end-2028 the network faces sustained float expansion from the Believers Fund (approximately 445M TON per year through October 2028) and the 1,081M TON whale freeze release on 21st February 2027. Combined, this implies average annual float growth in the high single digits to low double digits, against which a meaningful share of the nominal yield is compensation rather than real return. Post-2028, with both unlock streams complete and only residual emission inflation of approximately 0.6% remaining, the real and nominal yields converge. For modelling purposes the through-2028 real carry should be treated as roughly half the headline figure; the post-2028 carry approximates the headline.

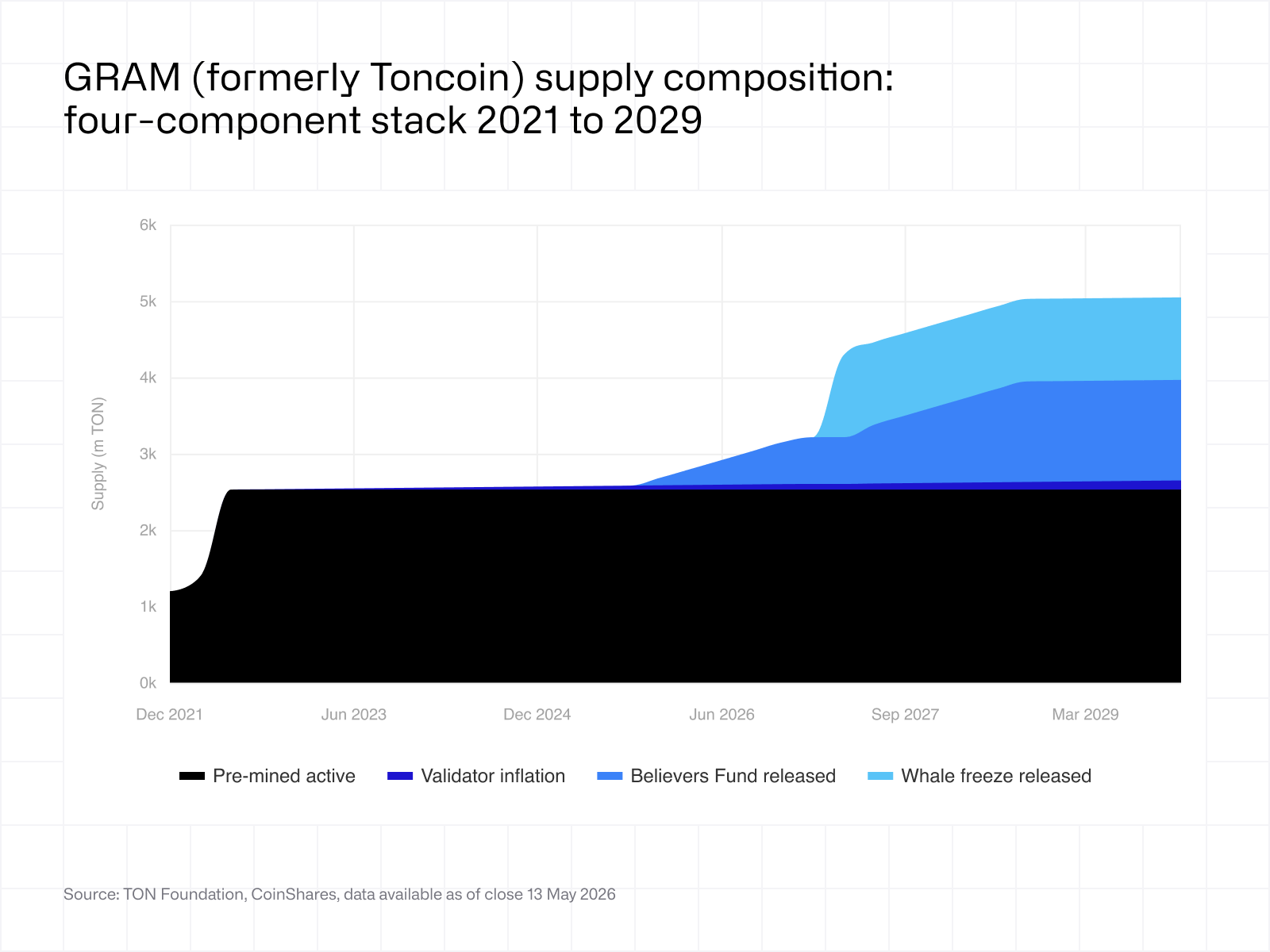

The most material supply consideration is the unlock of approximately 1.08 billion GRAM, or roughly 21% of total supply, that was voted to be frozen in early 2023 to mitigate whale-concentration risk. Starting in October 2025, around 37 million GRAM enters circulation every 30 days across 36 monthly installments, ending in late 2028. At a US$2.40 spot price this represents roughly US$90M of monthly supply pressure. This is the single most important calendar-driven risk in GRAM's tokenomics, and we incorporate it into the valuation framework explicitly in Section 6.

Total supply currently sits at approximately 5.18B, with circulating supply of around 2.7B, giving a fully diluted valuation of approximately US$12.5B against a circulating market capitalisation of US$6.5B.

Total supply currently sits at approximately 5.18B, with circulating supply of around 2.7B, giving a fully diluted valuation of approximately US$12.5B against a circulating market capitalisation of US$6.5B.

5. Network economics

TON's transition from network restart to fee-generating Layer 1 is recent and uneven. The table below sets out annualised L1 transaction fees and the principal drivers in each period.

2024 was the inflection point. CoinGecko's annual fee study ranked TON 10th globally at US$35.3M, a step change from outside the top tier the year before. The catalyst was the formalisation of the Telegram integration: Telegram's announcement in February 2024 that channel-owner ad revenue would settle in GRAM, the May 2024 launch of native USDT on TON, and the mini-app explosion led by Notcoin and Hamster Kombat. By late 2024 weekly DEX volume on TON had risen from approximately US$2M at the start of the year to over US$21M by year-end, a tenfold increase, and TVL had peaked at approximately US$740M in July.

2024 was the inflection point. CoinGecko's annual fee study ranked TON 10th globally at US$35.3M, a step change from outside the top tier the year before. The catalyst was the formalisation of the Telegram integration: Telegram's announcement in February 2024 that channel-owner ad revenue would settle in GRAM, the May 2024 launch of native USDT on TON, and the mini-app explosion led by Notcoin and Hamster Kombat. By late 2024 weekly DEX volume on TON had risen from approximately US$2M at the start of the year to over US$21M by year-end, a tenfold increase, and TVL had peaked at approximately US$740M in July.

For context, in 2024 Ethereum captured US$2.48B in L1 fees, Tron US$2.15B, Bitcoin US$923M, Solana US$751M, and BB Chain US$195M. TON's fee earnings remained roughly an order of magnitude below the largest Layer 1s despite stronger headline user growth, reflecting the dominance of free-to-use tap-to-earn applications and the low average per-transaction value inside mini-apps.

Cumulative throughput tells the same story from a different angle. Approximately US$184.3B, or 87% of all historical TON transaction value, was processed across 2024 and 2025, alongside roughly 2.59B transactions, or 80% of all historical activity. The network is, in volume terms, almost entirely a post-Telegram-integration story.

Telegram's parent revenue is the other side of the same coin. Group revenue grew approximately 65% year on year to US$870M in H1 2025, of which the exclusive TON partnership contributed approximately US$300M. This figure illustrates that the commercial relationship between the platform and the chain is already material, even if very little of it currently accrues to the TON token itself.

The May 2026 fee cut breaks the historical L1 revenue trajectory deliberately. Daily chain fees post-cut sit at roughly US$3,600, equivalent to approximately US$1.3M annualised. This is a strategic choice: Telegram and the TON Foundation have prioritised micro-transaction viability over near-term fee capture, accepting a step down in protocol revenue in exchange for removing the single most cited barrier to mass adoption. The implication is that TON is consciously prioritising adoption and scale ahead of monetisation. That changes the nature of the asset: less a present cash-flow claim, more an option on future monetisation policy. Whether transaction volume growth offsets the per-unit cut is the key empirical question over the next four to eight quarters. A tenfold volume increase returns the network to approximately US$13M of annualised fees; a fiftyfold or hundredfold increase, in line with the design intent of Telegram-native micro-payments, comfortably exceeds the 2024 high.

Two further data points frame the value-capture debate. First, DefiLlama's annualised gross fees across the TON ecosystem (including DEXs and application-level activity, not just L1) sit at approximately US$391.7M, but token-accruing protocol revenue is currently around US$1.1M, a capture ratio below 0.3%. Second, app-level revenue inside TON via Telegram Stars and in-app purchases is scaling, but the token's exposure to that economy will depend on whether fees are eventually restored once activity stabilises, or whether value capture migrates from L1 fees to validator income, staking yield, and Telegram-aligned revenue-sharing.

6. Valuation

Rating: Constructive / Positive on a 12-month view (high-conviction tactical, limited sizing). Spot price US$2.40. Base case 12-month target US$3.50 (+46%).

Headline view. TON has solved distribution better than any Layer 1 to date. It has not yet proven monetisation, retention or token-level value capture. The 12-month investment case rests on whether that gap closes. The May 2026 fee cut means TON is less a present cash-flow claim and more an option on future monetisation policy. Three credible value-accrual mechanisms (fee restoration once activity stabilises, an explicit revenue-sharing arrangement with Telegram, or migration of Telegram Stars settlement onto TON as primary rail) are discussed in Section 7. None is currently committed.

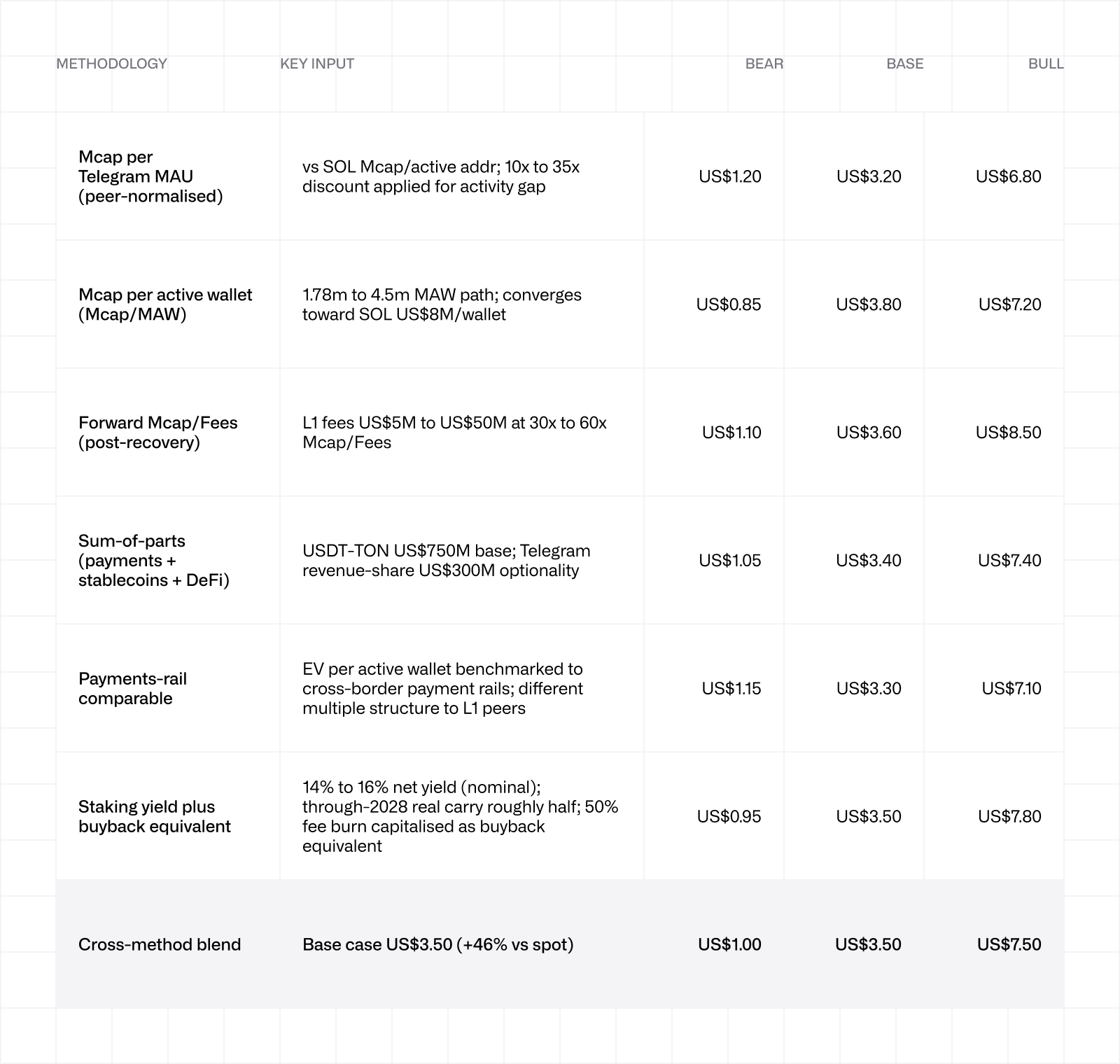

Methodology framework

All five methodologies share a common dependency on the same causal chain: Telegram MAU translates into an economically reachable subset, which converts to active TON wallets, which generates transaction activity, which produces fee revenue, which (subject to value-capture mechanisms) accrues to token holders. The methodologies are therefore consistency checks against each other rather than independent triangulation. We weight them equally in the base case and skew to forward and distribution-based metrics over trailing fee multiples, because the May 2026 fee cut compressed L1 fees from a 2024 base of US$35.3M to an annualised US$1.3M, taking trailing Mcap/Fees to a level that is mathematically meaningful but economically misleading.

The base cases cluster between US$3.20 and US$3.80. Because the underlying drivers are correlated rather than independent, this narrow dispersion should be read as internal consistency, not as a confidence interval. The genuine uncertainty band is the bear-to-bull spread of US$1.00 to US$7.50, which reflects regime shifts in the conversion ratio and the persistence of the fee compression rather than measurement noise. This is the right shape for a single-catalyst-bet network: the methodology choice matters less than the macro and adoption regime assumption.

The base cases cluster between US$3.20 and US$3.80. Because the underlying drivers are correlated rather than independent, this narrow dispersion should be read as internal consistency, not as a confidence interval. The genuine uncertainty band is the bear-to-bull spread of US$1.00 to US$7.50, which reflects regime shifts in the conversion ratio and the persistence of the fee compression rather than measurement noise. This is the right shape for a single-catalyst-bet network: the methodology choice matters less than the macro and adoption regime assumption.

Supply absorption framework

The unlock calendar belongs partly inside the valuation framework, not solely inside the risk section. At spot, the Believers Fund releases approximately US$90M of GRAM monthly through to October 2028. The 21st February 2027 whale freeze adds 1,081M TON in a single event (approximately US$2.6B at spot), which the market must absorb either at the release point or progressively as recipients distribute. For the token to sustainably re-rate, recurring demand must absorb this supply.

We track four absorption sources against the monthly supply figure. Treasury accumulation through TONX and successor vehicles is running at approximately 2.7 million GRAM per month based on the stated 250M GRAM target against today's 217.5M holding, equivalent to roughly US$6M to US$7M at current spot. European-listed ETP flows remain modest in single-digit US$m monthly. Stablecoin-driven on-chain activity contributes indirectly through gas-fee demand rather than direct token absorption. The staking sink, currently at a 9% ratio against a major Layer 1 average of 30% to 60%, has significant upside capacity but modest realised monthly absorption.

Aggregate observable monthly absorption is in the US$30M to US$50M range against US$90M of monthly unlock supply. The implication is a structural supply overhang during the Believers Fund release period, which the February 2027 whale freeze cliff materially worsens. This is the primary reason our base case sits at US$3.50 rather than at the upper end of the methodology range, despite the cross-method cluster pointing to fair value above spot.

The framework also defines what to monitor. The bull-case threshold is aggregate monthly absorption crossing approximately US$90M to US$120M for at least two consecutive quarters. The bear-case escalation is sustained absorption below US$50M, which is the bearish catalyst threshold in our watch list.

Snapshot and peer position

Three observations from the snapshot drive the rating. First, TON trades at approximately 12% of Solana's market capitalisation on roughly comparable user reach, but captures only 1.6% of Solana's TVL and a fraction of its fee economy. This is the source of the upside option value. Second, the Mcap per Telegram MAU of US$6.50 sits well below the implied equivalent for Solana (where active-address-based proxies yield well over US$200 per address). The gap closes structurally only if Telegram users convert to TON wallet holders at materially higher rates. Third, the staking ratio of 9% is materially below Solana (66%) and Ethereum (28%); upside re-rating from staking infrastructure deepening is therefore part of the bull case rather than already in the price.

Three observations from the snapshot drive the rating. First, TON trades at approximately 12% of Solana's market capitalisation on roughly comparable user reach, but captures only 1.6% of Solana's TVL and a fraction of its fee economy. This is the source of the upside option value. Second, the Mcap per Telegram MAU of US$6.50 sits well below the implied equivalent for Solana (where active-address-based proxies yield well over US$200 per address). The gap closes structurally only if Telegram users convert to TON wallet holders at materially higher rates. Third, the staking ratio of 9% is materially below Solana (66%) and Ethereum (28%); upside re-rating from staking infrastructure deepening is therefore part of the bull case rather than already in the price.

Position sizing guidance

Given the single-platform dependency, the supply unlock calendar, and the asymmetric outcome distribution, TON does not belong in a Bitcoin-substitute allocation slot. It is more appropriately framed within the selective altcoin sleeve of an institutional crypto allocation: a limited exposure in a diversified mandate, sized against the bear scenario rather than the base. The position complements rather than competes with Solana exposure, given the orthogonal user bases (Western retail and DeFi for Solana; messaging and emerging-market payments for TON). Allocators with a Bitcoin core, Solana satellite framework should view TON as an additional satellite with explicitly different beta drivers.

7. Telegram and TON: value accrual and misconceptions

Telegram (the private company) and the TON network (a public blockchain whose native token is GRAM (formerly Toncoin)) are legally and economically separate entities. The market frequently conflates them, particularly after the 4th May 2026 governance consolidation, and that conflation is the source of several of the largest analytical errors in TON valuation. The relationship is best understood as platform-to-infrastructure: Telegram is the distribution and demand-side; TON is the settlement layer.

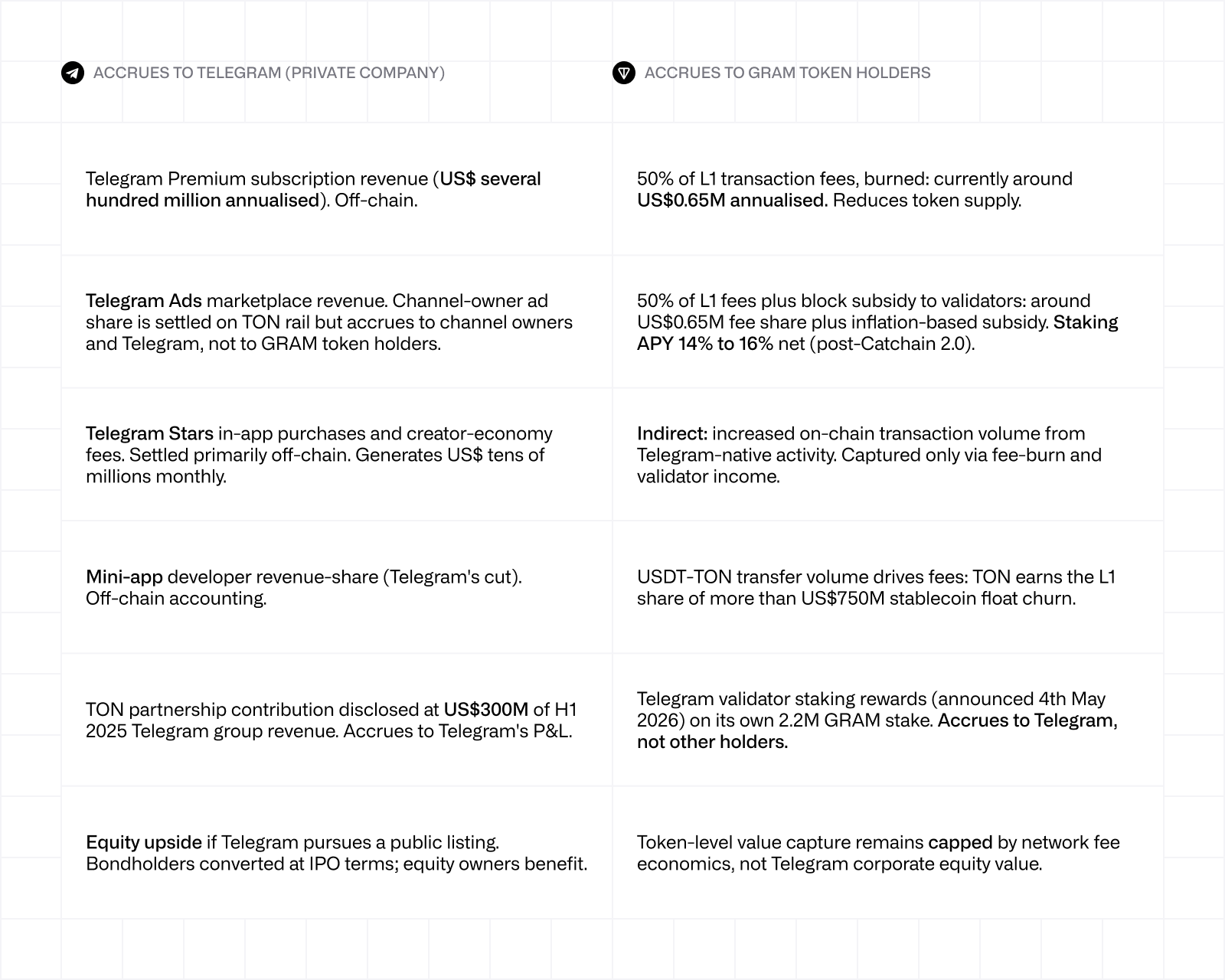

The clearest way to delineate the linkage is to trace where revenue actually accrues.

The asymmetry is stark. Telegram's annualised group revenue of approximately US$1.7B (extrapolated from H1 2025) flows to a privately-held company with convertible debt outstanding and a possible future listing. TON's annualised token-accruing revenue, comprising L1 fee burn and validator income, is approximately US$1.3M gross, or roughly 0.08% of Telegram's group revenue. The two numbers are linked operationally but not financially: more Telegram activity drives more TON transactions, which marginally increases fee burn, but the bulk of the commercial value remains inside Telegram.

The asymmetry is stark. Telegram's annualised group revenue of approximately US$1.7B (extrapolated from H1 2025) flows to a privately-held company with convertible debt outstanding and a possible future listing. TON's annualised token-accruing revenue, comprising L1 fee burn and validator income, is approximately US$1.3M gross, or roughly 0.08% of Telegram's group revenue. The two numbers are linked operationally but not financially: more Telegram activity drives more TON transactions, which marginally increases fee burn, but the bulk of the commercial value remains inside Telegram.

Common misconceptions

1. "Owning TON is equivalent to pre-IPO Telegram equity." Incorrect. TON has no claim on Telegram's revenue, profits, or equity. The two are operationally interdependent but capital-structurally separate. A Telegram IPO would not directly distribute value to TON holders, although secondary effects (publicity, validation of the partnership) could re-rate the token.

2. "Telegram ad revenue settling in GRAM means TON captures the ad market." Incorrect. Ad revenue is denominated and settled on TON rails, but the underlying revenue accrues to Telegram and to channel owners. The TON network captures only the marginal transaction fee on the settlement, which is sub-cent per transaction post fee cut.

3. "Telegram becoming the largest validator aligns its interests with GRAM token holders." Partially correct, but the alignment is operational rather than financial. Telegram earns staking rewards on its own stake; other holders do not share in those rewards. The alignment is that Telegram now has a direct operational reason to grow the network, not that it has signed a revenue-sharing agreement with holders.

4. "Mini-app revenue (Hamster Kombat, Catizen, Notcoin, etc.) flows through TON." Largely incorrect. The bulk of mini-app monetisation runs through Telegram Stars, an off-chain credits system, with TON used selectively for token launches and on-chain settlement. The token accrual is incidental, not structural.

5. "Fee burn means GRAM is deflationary like ETH post-Merge." Not currently, and the framing misses a larger point. On a true-inflation basis, validator emissions of approximately 95M GRAM per year (about 0.6% of total supply) materially exceed annualised L1 fee burn of approximately US$0.65M (around 0.3M GRAM), making net emission positive by two to three orders of magnitude.

More importantly, the binding supply consideration is not emission but unlocks: the Believers Fund releases approximately 445M TON per year through October 2028 and the whale freeze releases 1,081M GRAM in a single event on 21st February 2027. These are not inflation in the technical sense (the tokens already exist) but they represent the dominant source of dilution facing token holders. Comparing TON to post-Merge Ethereum on deflation grounds is therefore doubly misleading: emission is positive, and economic dilution from unlocks is several orders of magnitude larger than fee-burn dynamics. The 50% fee burn becomes economically meaningful only at L1 fee levels well above the 2024 peak and once the unlock calendar is materially through.

What would change the picture

Three observable developments would shift value accrual materially in favour of the token. First, an explicit revenue-sharing arrangement between Telegram and TON validators or holders, structured along the lines of a perpetual licence fee or a fee-sharing waterfall, which is technically feasible but has not been proposed. Second, migration of Telegram Stars settlement onto TON as the primary rail rather than as one of several payment methods; this would transform the volume-to-token-revenue conversion ratio. Third, restoration of L1 fees above pre-cut levels alongside an order-of-magnitude increase in transaction volume; in this scenario, fee-burn becomes a credible buyback equivalent at 2% to 4% of market capitalisation annually.

Until at least one of these developments occurs, TON should be modelled as infrastructure exposure to a Telegram-driven payments and mini-app economy, not as a synthetic equity stake in Telegram itself. This distinction is the single most important framing for institutional position sizing, and it underpins our preference for distribution-based and sum-of-parts valuation methodologies over direct revenue multiples.

8. Investment case and comparative positioning

The structural case for TON rests on three points.

First, distribution is the strongest in crypto. No other Layer 1 has an embedded user base of one billion at the application layer. TON does not need to compete for users, only for activity. Customer acquisition costs for Telegram-native applications are reportedly 90% to 95% lower than traditional app-store equivalents, with several mini-apps (Notcoin, Hamster Kombat, Catizen) each reaching tens to hundreds of millions of users.

Second, the technical envelope after Catchain 2.0 supports payment use cases that the prior architecture could not. Sub-second finality and base fees of US$0.0005 sit below the threshold typically required for micro-transactions, tipping, and per-action settlement, particularly for gaming and in-chat commerce. Telegram's mandate that blockchain-enabled mini-apps operate exclusively on TON further entrenches the network as the default settlement layer for in-app economic activity.

Third, institutional access is now in place. TON Strategy Company (Nasdaq: TONX) launched in August 2025 via a US$558M private placement to acquire approximately 217.5 million TON, of which more than 99% is staked as of Q1 2026 (221.2M of 221.9M TON holding). Following the April 2026 Catchain 2.0 upgrade, annualised staking revenue runs at approximately US$89M gross at current spot price, recycled into share buybacks. TON is now spot-listed on ETPs in Europe, Coinbase, Gemini, and Robinhood, alongside other tier-one venues.

Relative valuation provides the clearest framing.

Against Solana, TON trades at approximately 12% of market capitalisation despite comparable or higher user reach, partially offset by Solana's mature DeFi ecosystem, higher daily transactions, and broader developer base. Against Ethereum, TON trades at approximately 2% of market capitalisation; the gap reflects Ether's role as collateral, settlement layer, and staking yield benchmark, not direct application-layer competition.

Against Solana, TON trades at approximately 12% of market capitalisation despite comparable or higher user reach, partially offset by Solana's mature DeFi ecosystem, higher daily transactions, and broader developer base. Against Ethereum, TON trades at approximately 2% of market capitalisation; the gap reflects Ether's role as collateral, settlement layer, and staking yield benchmark, not direct application-layer competition.

The Solana comparison works directionally for distribution-adjusted valuation but should be handled carefully. Solana's market capitalisation reflects deeper DeFi liquidity, stronger developer reflexivity, broader institutional familiarity and a more crypto-native economic ecosystem. TON's structural profile may be closer to a messaging and payments settlement rail than to a general-purpose smart contract platform. Read on those terms, the appropriate peer set is not other Layer 1s but cross-border payments infrastructure (SWIFT, Visa Direct, Wise, and stablecoin settlement networks), which implies a different multiple structure and discount rate. We use the Solana benchmark to size the upside option in the bull case rather than to anchor central fair value. The likely steady-state peer set for TON is hybrid: settlement-rail valuation for the core business, general-purpose L1 valuation only for the optionality component.

Relative to peers TON now offers materially the highest staking yield among the major Layer 1s following the April 2026 Catchain 2.0 upgrade. At an approximate nominal net APY of 14% to 16%, TON sits well above Ethereum's 2.8% to 3.3% and approximately 2x to 3x Solana's 6.5% to 7.5%. The carry advantage is the most material change to the TON investment case in the past quarter and has elevated TON to the top of the Layer 1 yield curve. The qualification, as noted in Section 4, is that through-2028 real economic carry is materially lower than the nominal figure once unlock dilution is accounted for. Even after that adjustment, TON's risk-adjusted carry remains comfortably above the major Layer 1 peer set.

9. Risks

Single-platform dependency. TON's investment case is, in practice, a Telegram investment case. Any regulatory action against Telegram, a founder-specific event, or strategic shift would transmit directly to TON value. Pavel Durov's August 2024 arrest in France illustrated this concentration. The May 2026 governance consolidation increases it further.

Supply unlock pressure. The rolling unlock of frozen tokens described above will continue to weigh on supply through to early 2029, with observable absorption running at roughly half the monthly supply figure. The 21st February 2027 whale freeze cliff is the single largest discrete event. At periods of weak risk appetite this is likely to be the dominant short-term price driver.

Activity to distribution gap. If monthly active wallet conversion fails to scale meaningfully beyond current levels, the TON thesis reduces to a treasury-and-narrative trade rather than a fundamentals trade. TVL well below the 2024 peak underlines the gap.

Fee compression. The May 2026 fee cut is a deliberate trade-off. If transaction volume growth does not at least match the per-unit reduction within the next eight quarters, the network risks structurally lower fee earnings without compensating volume, weakening the token-level value-capture argument.

Validator concentration. Telegram's direct entry as the largest validator, while improving execution capacity, narrows the validator distribution and weakens the decentralisation argument.

Quantum exposure. Broad concerns around the quantum vulnerability of current elliptic-curve cryptography apply to TON in common with Ethereum and Solana, and warrant attention as part of any long-horizon allocation framework.

10. Political and regulatory vulnerabilities

TON carries a more concentrated political risk profile than any major Layer 1. The combination of a Russian-born founder under active French criminal investigation, a platform with documented links to actors on multiple sanctioned-entity lists, a US regulatory history that includes a 2020 settlement with the SEC, and a governance consolidation that now ties the chain operationally to a single private company makes political risk a first-order consideration for institutional positioning rather than a residual risk-management item.

Founder and key-person risk

Pavel Durov was arrested at Le Bourget Airport on 24th August 2024 and indicted on 12 charges, including complicity in the distribution of child sexual abuse material, drug trafficking, organised crime facilitation, and unlawful operation of an encrypted messaging service. Each charge carries a maximum penalty of approximately ten years. French authorities lifted his travel restrictions on 13th November 2025, but the criminal investigation remains active and unresolved as of May 2026. Durov has publicly accused the French government of suppressing free speech and stated that he faces over a dozen ten-year charges, framing his case as politically motivated. The case has no scheduled trial date.

Three scenarios merit institutional consideration. First, the case settles or is dismissed without indictment to trial: neutral to mildly positive for TON. Second, the case proceeds to trial with a conviction or plea: materially negative for both Telegram and TON, particularly if it triggers a leadership transition or forced re-domiciliation. Third, Durov is forced to comply with European data-disclosure requirements at scale: negative for Telegram's positioning with privacy-focused user bases but potentially positive for institutional acceptance of TON. The asymmetry of the outcome distribution argues for explicit position-size constraints rather than scenario-weighted modelling.

Platform regulatory exposure

Telegram operates under increasing regulatory pressure across multiple jurisdictions. Following Durov's arrest, the platform updated its terms of service in September 2024 to permit disclosure of user IP addresses and phone numbers to authorities with valid legal requests. Telegram has subsequently reported blocking over 34 million groups and channels in 2025 alone. The EU Digital Services Act (DSA) applies, and Telegram's contested user-count disclosure (claimed below the 45 million EU threshold for Very Large Online Platform designation) remains a flashpoint. Compliance with the UK Online Safety Act and EU Markets in Crypto-Assets regulation (MiCA, applicable to TON-denominated activity) is similarly contested.

Telegram is fully blocked or significantly restricted in China, Iran, Pakistan, Saudi Arabia, and intermittently in several other jurisdictions. Each ban functionally removes TON's distribution case in that market.

Russia and sanctions-transmission risk

Telegram has approximately 60 to 70 million Russian users and is one of the principal communication platforms used by Russian military and propaganda networks alongside Ukrainian government and civilian users. The platform is used by sanctioned entities (Hamas, Hezbollah, and various designated criminal organisations) for coordination and recruitment. Neither Telegram as a platform nor TON as a network has been designated by US Treasury OFAC, the UK OFSI, or the EU. The relevant institutional question is the probability and consequence of a designation.

Three sanctions-transmission paths warrant monitoring. First, direct designation of Telegram on platform-facilitation grounds, which would force exchange delistings and broker-dealer divestment. Second, designation of specific TON addresses or smart contracts linked to sanctioned activity, in the manner of OFAC's August 2022 designation of the Tornado Cash mixer, which would impose compliance friction on the entire chain. Third, secondary sanctions on Tether following its US$750M USDT-TON stablecoin float, which has historically been less filtered than USDT on Ethereum or Tron. Each path is currently low-probability but not negligible, and each would materially impair institutional access.

US regulatory history and current position

The US regulatory record on TON is unusually long for a Layer 1. In October 2019 the SEC obtained a temporary restraining order halting the original Telegram-led TON launch (the Gram token), and in June 2020 Telegram settled by returning approximately US$1.2B to investors and paying an US$18.5M civil penalty. The current TON network was relaunched in 2020 by the open-source community without Telegram's direct involvement, and the present token (GRAM (formerly Toncoin)) is legally distinct from the abandoned Gram. Nonetheless, the regulatory memory persists, and any future SEC enforcement leadership change could revisit the network's status.

The current US framework is more constructive. TON is spot-listed on Coinbase, Gemini, and Robinhood, and the TON Strategy Company (Nasdaq: TONX) was approved as a publicly listed digital asset treasury vehicle in August 2025. The Trump administration's broader crypto policy stance and the legislative progress of the CLARITY Act through 2026 reduce near-term enforcement risk materially. The principal residual exposure is CFTC jurisdictional treatment of Telegram's prediction-market and channel-monetisation activities, which is unresolved.

Governance jurisdictional concentration

The TON Foundation is incorporated in Switzerland, which provides a more stable regulatory base than the original Cayman structure or the abandoned BVI vehicle. The 4th May 2026 announcement that Telegram (FZ-LLC, registered in Dubai) would take over principal operating responsibilities introduces a UAE regulatory dependency alongside the Swiss foundation structure. The UAE has been broadly crypto-permissive, but the combination of Swiss foundation, UAE operating company, French legal exposure to the founder, and Russian-language community concentration means that material regulatory action in any one of four jurisdictions could affect the network. No other major Layer 1 has comparable jurisdictional spread.

Operational mitigants

Several factors reduce the political risk transmission to TON specifically. The token is held in a globally distributed validator set rather than at Telegram's level, and the protocol continues to operate independently of any single corporate entity. The TON Foundation has demonstrated capacity to coordinate technical upgrades without Telegram's direct involvement (the May 2024 USDT launch, the August 2025 institutional treasury launch). Institutional wrappers including TONX provide a regulated access layer that would survive most non-existential platform-level events. And the May 2026 governance consolidation, while increasing platform dependency, also formalises Telegram's operational commitment in a way that reduces the abandonment risk that has historically been the worst-case scenario for community-stewarded chains.

On a net basis, political and regulatory risk is the second-largest non-fundamental risk factor for TON after the supply unlock calendar, and the two are correlated. Institutional positioning should reflect the asymmetric distribution: tail-risk events on the political axis are low-frequency but high-severity, and conventional volatility-based sizing would understate the appropriate position constraint. The note's 1% to 3% selective-altcoin-sleeve guidance is calibrated with these political factors as an explicit input.

11. Catalysts (12-month watch list)

Bullish

Weekly DEX volume above US$200M for four consecutive weeks (currently c.US$42M). Signals that fee compression is being offset by volume growth and validates the base-to-bull transition.

Aggregate monthly absorption above US$90M to US$120M for two consecutive quarters. The single highest-information variable in the supply-demand framework.

TONX treasury growth above 250M TON (currently c.217.5M). Indicates sustained institutional accumulation independent of price action.

Monthly active wallet conversion ratio above 1% of Telegram MAU (currently c.0.12%). The binding variable in the causal chain.

Validator vote in June 2026 on reducing block rewards/inflation passes constructively.

Bearish

Adverse regulatory action against Telegram in the US or EU. Founder-specific or platform-specific risk events transmit directly.

Frozen token unlock supply pressure unabsorbed: monthly net inflows to TON below US$50M against US$90M of unlock-driven supply.

TVL fails to recover above US$200M by year-end 2026 despite the fee cut, indicating the trade-off has not produced the intended activity response.

Durov case escalation to trial date, adverse procedural ruling, or new charges. Single-name founder risk transmits directly to the network through governance and platform exposure.

Sanctions transmission event: OFAC, OFSI, or EU action against Telegram, the TON Foundation, or specific TON addresses linked to designated actors.

Conclusion

TON sits in an unusual position for an institutional allocator. It has the largest user-facing distribution channel in the industry, a clearly visible step change in network economics through 2024, the technical envelope after Catchain 2.0 to support continued scale, and a Nasdaq-listed treasury vehicle providing regulated access. It also carries a 21% total-supply unlock running through 2029, a market capitalisation to TVL gap that requires significant activity growth to close, a now-deliberate compression of L1 fee revenue, and a concentration of governance and product control inside one platform.

The April 2026 Catchain 2.0 upgrade has materially recalibrated the investment case. Network gross staking yield stepped up to approximately 16.7% annualised, taking TON to the top of the Layer 1 yield curve and shifting carry from a marginal contributor to a meaningful component of total return. The base-case 12-month total return comprises 46% price appreciation to US$3.50 plus through-2028 real-economic-adjusted staking carry of approximately 4% to 8%, giving a blended return of around 50% to 54%.

The bull case is that the fee cut catalyses an order-of-magnitude expansion in transaction volume and that distribution finally converts to durable, multi-source revenue. In that scenario TON is materially mispriced against Solana on a user-adjusted basis, and the closest analogue is not a smart contract platform but a cross-border payments rail embedded inside the dominant messaging app outside the US and China. The bear case is that TON remains a high-distribution, low-conversion network whose token captures little of the platform's value. Our base case 12-month target is US$3.50, sized as a selective altcoin satellite (within a diversified institutional crypto mandate) rather than a core position. The position complements rather than competes with Solana exposure, given orthogonal user bases.