Just the right amount of Bitcoin

![]() 5 Min. Lesezeit

5 Min. Lesezeit

- Finanzen

- Bitcoin

In our last piece we established that bitcoin enhances risk adjusted returns in a traditional 60/40 equity/bond portfolio. Here we ask, ‘Historically, what’s the right amount of bitcoin?’

Our research indicates that:

Small weightings of bitcoin have had an outsized positive impact on both risk-adjusted returns and diversification relative to other alternative assets.

Increasing risk (annualised volatility of the portfolio) by 1.2% suggests a portfolio weight of just under 4% in a traditional 60/40 equity/bond portfolio.

Quarterly rebalancing of Bitcoin back to the original invested weight helps contain volatility.

Bitcoin has been a volatile asset since its inception in 2009, keeping some investors wary of investing. We believe, with relatively limited risk, an allocation to Bitcoin can be made that has a meaningful impact on portfolio performance.

In this article, we highlighted the potential diversification benefits that an allocation to bitcoin can provide to a traditional 60/40 equity/bond portfolio. In particular, Bitcoin’s lack of correlation to other assets potentially makes it a far more useful alternative asset for investors looking to reduce exposure to economic cycles, especially when compared to other popular alternative investments, such as gold or a broad basket of commodities.

So, how much should you invest in bitcoin?

Whilst there is no one-size-fits-all approach, we believe that Bitcoin is steadily evolving into a store of value, and a backtest of bitcoin price performance in a portfolio can still deliver valuable insights for long-term investors. We also believe that informing investors on the best Bitcoin portfolio allocation in their portfolio, according to their risk appetite, is essential.

To help investors understand how bitcoin can help or hinder a portfolio we created a database of daily returns starting from 2015 when the investors were first able to invest in the asset via an Exchange Traded Product (ETP). We started with a traditional balanced portfolio with 60% equities and 40% bonds and then added a notional amount of bitcoin, detracting from both equities and bonds equally.

As bitcoin is an asset in an early growth phase, most investors would allow its portfolio weight to drift to some extent. We decided to rebalance on a quarterly basis––despite its potential hindrance on enhancing returns––because we believe rebalancing helps moderate volatility. You can read more about the composition of this portfolio in this report.

Bitcoin Portfolio Allocation: Volatility

Adding Bitcoin to a portfolio does increase portfolio volatility. So how much should be added to a portfolio? There are several ways to approach this. One method is volatility targeting, and the chart below highlights how much Bitcoin in a portfolio contributes to risk.

As a guide, the chart highlights a 4% weighting in a portfolio would increase the overall portfolio volatility by just over 1%.

As a guide, the chart highlights a 4% weighting in a portfolio would increase the overall portfolio volatility by just over 1%.

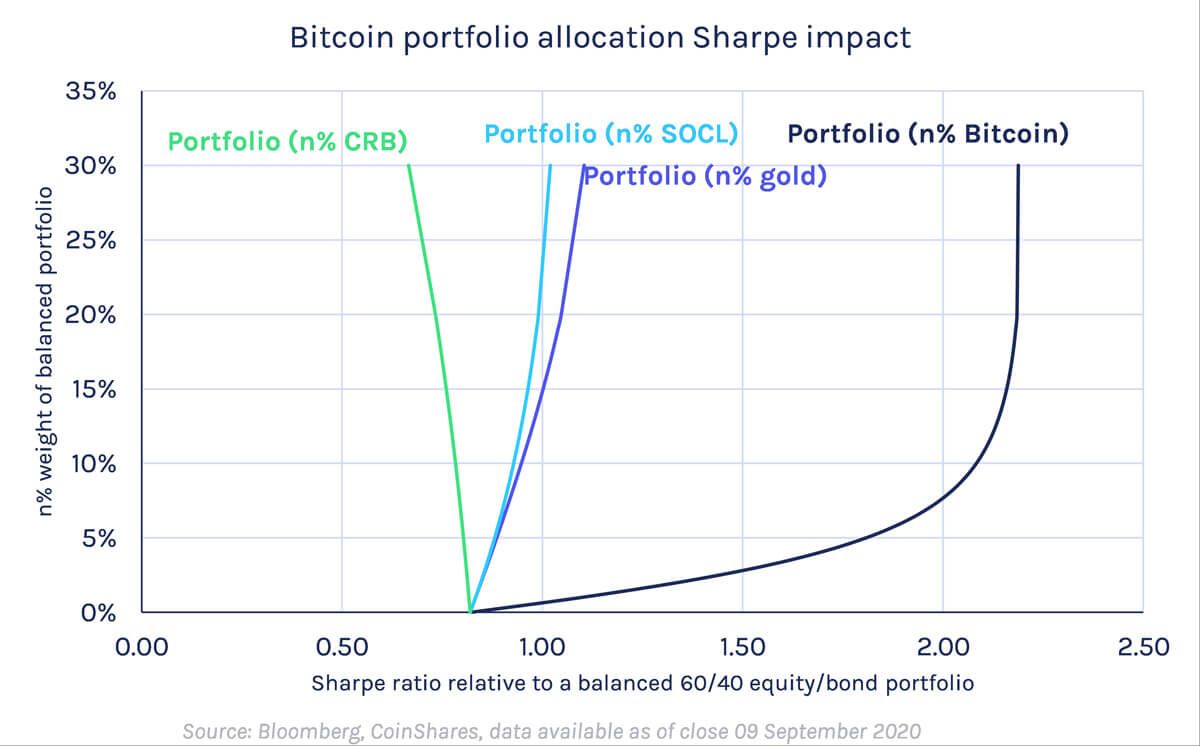

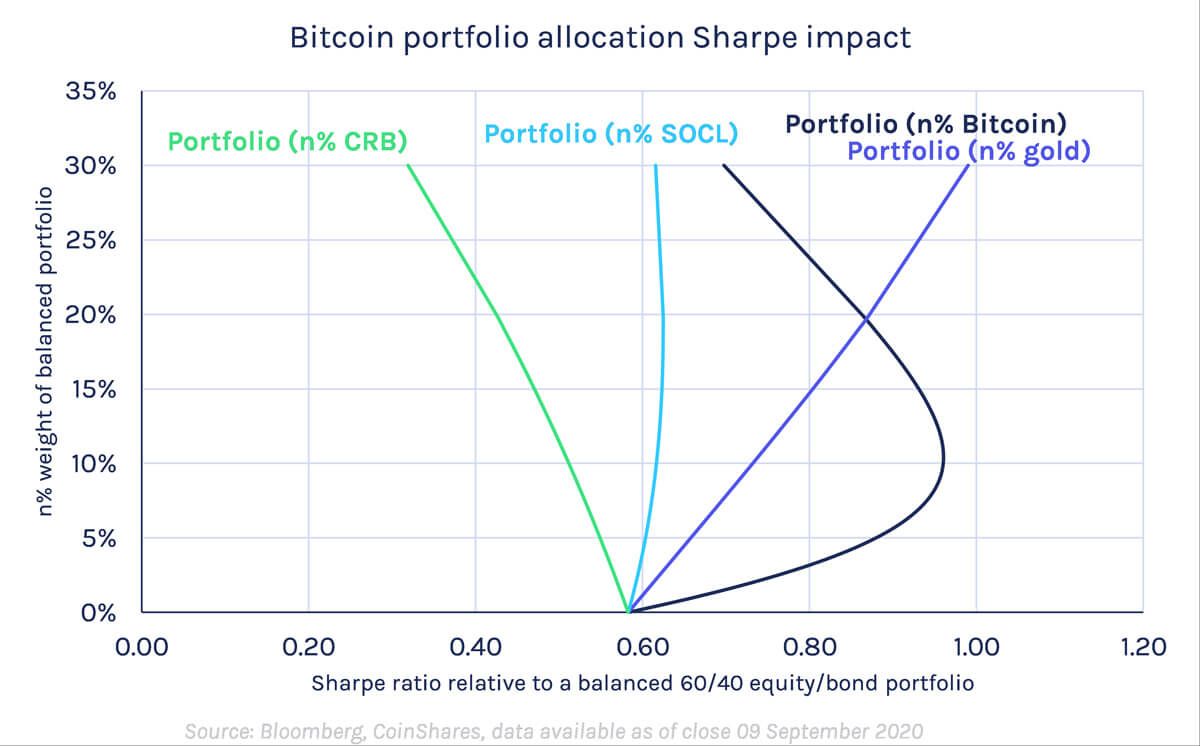

Bitcoin Portfolio Allocation: Sharpe Impact

An alternative approach is to blend the risk and reward by analysing the impact on the portfolio Sharpe ratio (a measure of returns relative to the level of risk taken on) in varying Bitcoin portfolio weights.

The backtested results over almost 5 years produce the above chart. Movement to the right indicates higher risk-adjusted returns while movement up reflects a higher allocation to bitcoin over the test period. This analysis indicates that the most significant improvements in the Sharpe ratio are gained through an allocation of up to 10% bitcoin in the portfolio. This highlights that even a small addition of bitcoin has a big impact on the Sharpe ratio. We have also included other comparable assets and indices over the same time period, and they have had little impact relative to bitcoin on the Sharpe ratio, even when extreme weights are applied.

The backtested results over almost 5 years produce the above chart. Movement to the right indicates higher risk-adjusted returns while movement up reflects a higher allocation to bitcoin over the test period. This analysis indicates that the most significant improvements in the Sharpe ratio are gained through an allocation of up to 10% bitcoin in the portfolio. This highlights that even a small addition of bitcoin has a big impact on the Sharpe ratio. We have also included other comparable assets and indices over the same time period, and they have had little impact relative to bitcoin on the Sharpe ratio, even when extreme weights are applied.

Investors could argue that this 5 year period is overly favourable, and given that Bitcoin rallied over this period any analysis would look great. To address this concern we also included analysis from the Bitcoin price peak on 18th December 2017 to date, a period where Bitcoin negatively contributes to overall returns. The results highlight that Sharpe ratios remain positive, although understandably not to the same degree. This may seem nonsensical but this is due to our quarterly rebalancing strategy, where Bitcoin is reset back to its original weighting every quarter. We have found that regular rebalancing can reduce potential for higher returns, but is prudent in containing Bitcoin’s volatility.

Gold has a similar impact in diversifying a portfolio, although portfolio weights above 20% are required to achieve any substantive impact on diversification. Bitcoin is converse to this, with minimal weights having a far greater impact.

Gold has a similar impact in diversifying a portfolio, although portfolio weights above 20% are required to achieve any substantive impact on diversification. Bitcoin is converse to this, with minimal weights having a far greater impact.

In conclusion, bitcoin’s investment characteristics have historically made it attractive both as a driver of returns and a portfolio diversifier. Compared to other common alternatives and diversifiers, bitcoin has delivered outsized positive impacts on returns, Sharpe ratio and diversification, even at very low allocation sizes.

As to answering the question:“how much should I invest in Bitcoin?” this very much depends on your appetite for risk. By our analysis, however, allowing a modest increase in overall portfolio volatility of 1.2% would suggest a Bitcoin portfolio weight of just under 4% in a traditional 60/40 equity/bond portfolio, although investors should always be mindfulto regularly rebalance back to the original investment weight.