Rapport trimestriel sur la finance hybride — T1

![]() 14 min de lecture

14 min de lecture

- Finance

- Bitcoin

- Données

Le premier rapport consacré à l'analyse de la finance hybride

La finance est en pleine reconfiguration. Ce qui se dessine est profond et durable : l'infrastructure des marchés de capitaux traditionnels et les rails on-chain convergent vers un système financier unifié. Des blockchains publiques règlent désormais des actifs institutionnels. Des gestionnaires d'actifs de Wall Street émettent des fonds sur Ethereum. Des plateformes de produits dérivés, générant des centaines de millions de dollars de revenus trimestriels, fonctionnent entièrement on-chain. Bitcoin a catalysé cette convergence en prouvant qu'un actif natif d'une blockchain pouvait gagner la confiance institutionnelle et s'imposer comme outil de diversification à grande échelle. La finance hybride est ce qui vient ensuite.

CoinShares définit la finance hybride comme l'intersection de trois forces structurelles : une infrastructure de règlement capable de supporter un poids économique réel ; la tokenisation d'actifs traditionnels (bons du Trésor, actions, matières premières) et des applications on-chain grand public générant des revenus réels et récurrents. Il ne s'agit pas de catégories spéculatives. Elles sont mesurables et elles progressent.

Cette première édition du rapport Finance Hybride de CoinShares, produite en collaboration avec Token Terminal, a pour ambition de faire passer la conversation du récit aux données, en appliquant un cadre analytique cohérent aux segments qui portent cette convergence et en suivant leur évolution trimestrielle. Le rapport couvre cinq segments empiriques : les stablecoins, les fonds tokenisés, les actions tokenisées, les matières premières tokenisées et les entreprises on-chain, avec un éclairage complémentaire sur les couches de règlement qui les sous-tendent.

Le calendrier n'est pas anodin. 2026 marque le moment où la finance hybride passe de tendance visible à structure de marché mesurable. L'offre totale de stablecoins a franchi les 297 milliards de dollars. Les encours des fonds tokenisés ont progressé de 181 % en glissement annuel. Une plateforme décentralisée de produits dérivés, Hyperliquid, a dégagé davantage de revenus trimestriels que de nombreuses bourses régulées. L'infrastructure n'est plus théorique. La question est désormais de savoir quelles plateformes, quels émetteurs et quelles chaînes parviendront à s'y construire des positions durables.

Ce rapport est la tentative de CoinShares et Token Terminal de répondre à cette question de manière systématique, trimestre après trimestre.

Ethereum domine le règlement, tandis qu’Hyperliquid se distingue par ses revenus

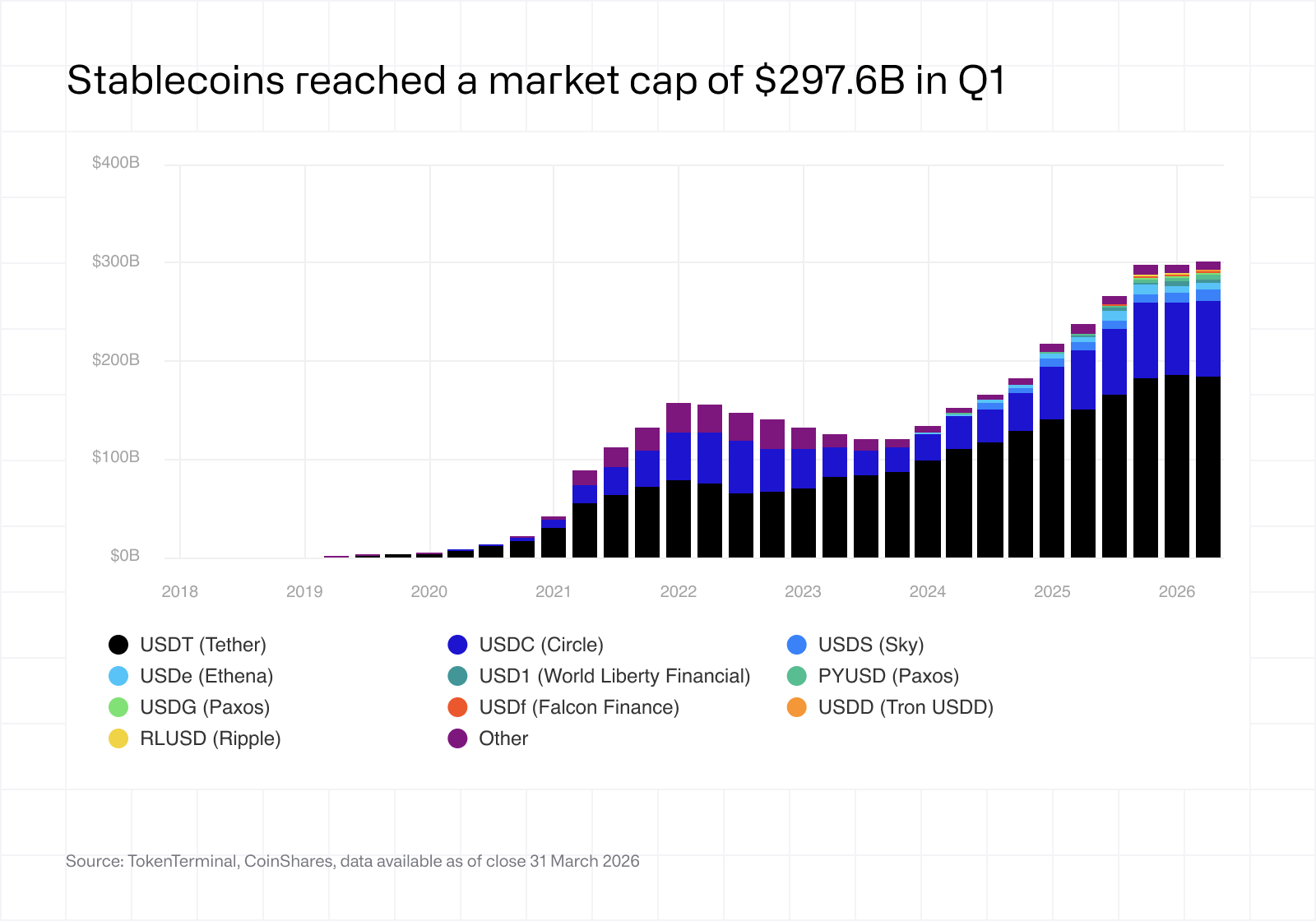

Stablecoins

Les stablecoins1 constituent la couche fondamentale de la finance hybride, en tant qu'équivalents on-chain des monnaies fiduciaires. Ils sont principalement utilisés pour le trading, les paiements et comme collatéral au sein des applications financières on-chain.

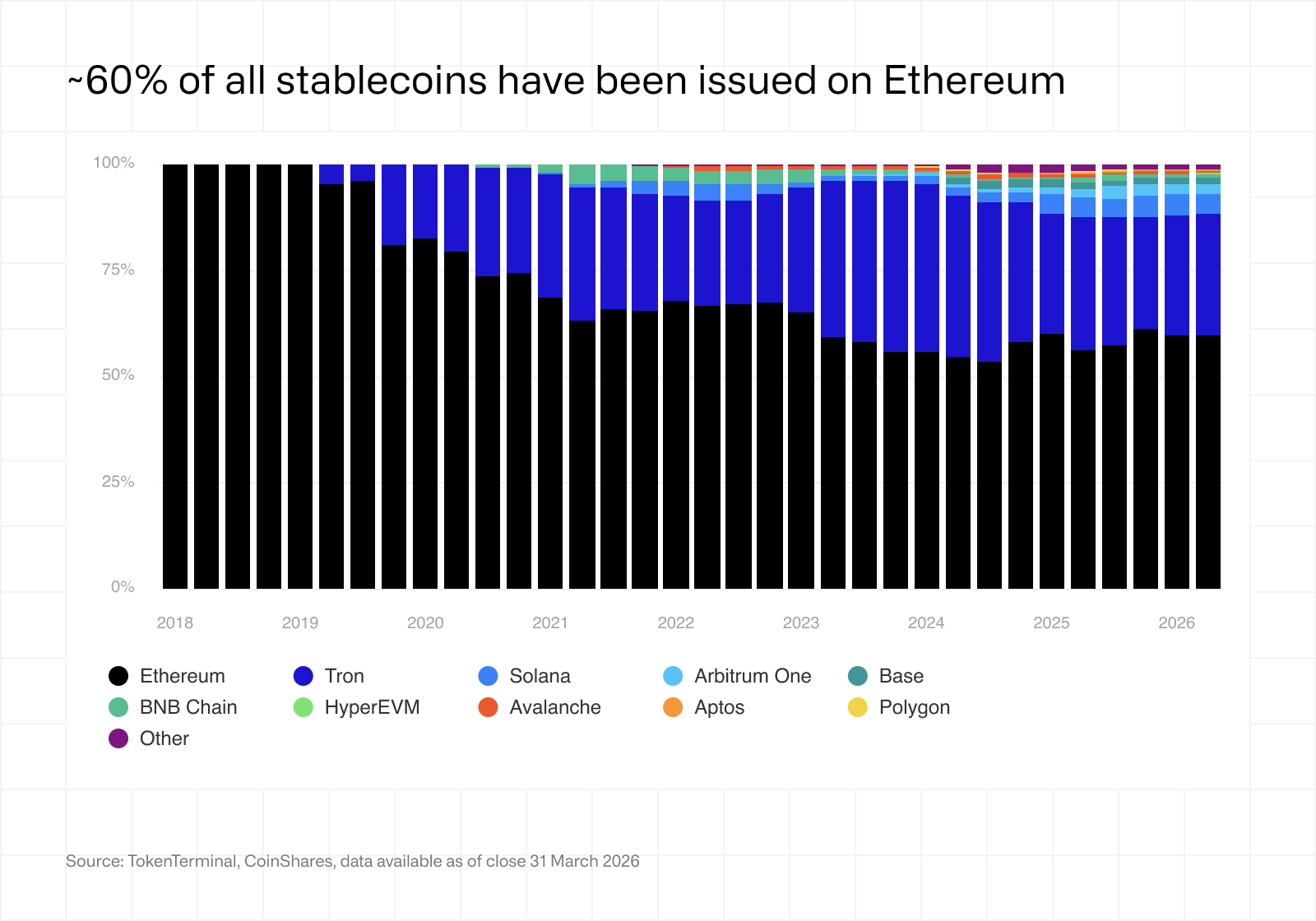

Au premier trimestre, le marché des stablecoins a atteint 297,6 milliards de dollars de capitalisation on-chain, consolidant sa position de segment le plus important et le plus mature de la finance hybride. La progression atteint 37,2 % en glissement annuel, même si le marché marque le pas depuis le T4 2025 (+0,2 %). Le leadership reste concentré chez les émetteurs natifs du secteur crypto - Tether, Circle, Sky2, Ethena et Paxos. Environ 60 % des stablecoins en circulation sont émis sur Ethereum, tandis que l'activité progresse sur Tron, Solana, Arbitrum et Base.

Fonds tokenisés

Les fonds3 tokenisés étendent la gestion d'actifs traditionnelle à l'environnement on-chain, permettant aux investisseurs d'accéder à des produits financiers structurés avec une transparence et une composabilité accrues.

Au premier trimestre, les fonds tokenisés ont atteint 9 milliards de dollars d'encours on-chain, soit une hausse de 181,3 % en glissement annuel et de 12,6 % par rapport au T4 2025, ce qui en fait l'un des segments à la croissance la plus rapide de la finance hybride. Une part significative de cette croissance est portée par des stratégies tokenisées adossées à des instruments de dette américaine à court terme, traduisant une forte demande pour des actifs on-chain peu risqués et générateurs de rendement. Le marché reste concentré autour d'un petit nombre d'émetteurs de Wall Street (BlackRock, Franklin Templeton, etc.), ainsi que d'émetteurs natifs de la crypto comme Circle et Ondo, près de 50 % de l'ensemble des émissions étant concentrées sur Ethereum.

Actions tokenisées

Les actions tokenisées4 représentent la migration des actions cotées et non cotées vers une infrastructure blockchain, permettant la propriété fractionnée et la négociation en continu. Ces instruments visent à reproduire l'exposition aux actions traditionnelles tout en introduisant programmabilité et accessibilité mondiale.

Au premier trimestre, le marché des actions tokenisées a atteint 773,3 millions de dollars de capitalisation on-chain, témoignant d'un segment encore émergent mais en croissance rapide : quasi inexistant il y a un an (27,6 millions de dollars), sa capitalisation a bondi de 2 697 % en glissement annuel, dans la continuité d'une forte progression au T4 2025 (504,1 millions de dollars). Cette croissance a été principalement portée par des émetteurs natifs de la crypto, tels qu'Ondo Finance et xStocks. Environ 50 % des actions tokenisées sont émises sur Ethereum, le reste étant réparti entre Solana, BNB Chain et Arbitrum, cette dernière étant également la couche de règlement sur laquelle Robinhood a émis des milliers d'actions.

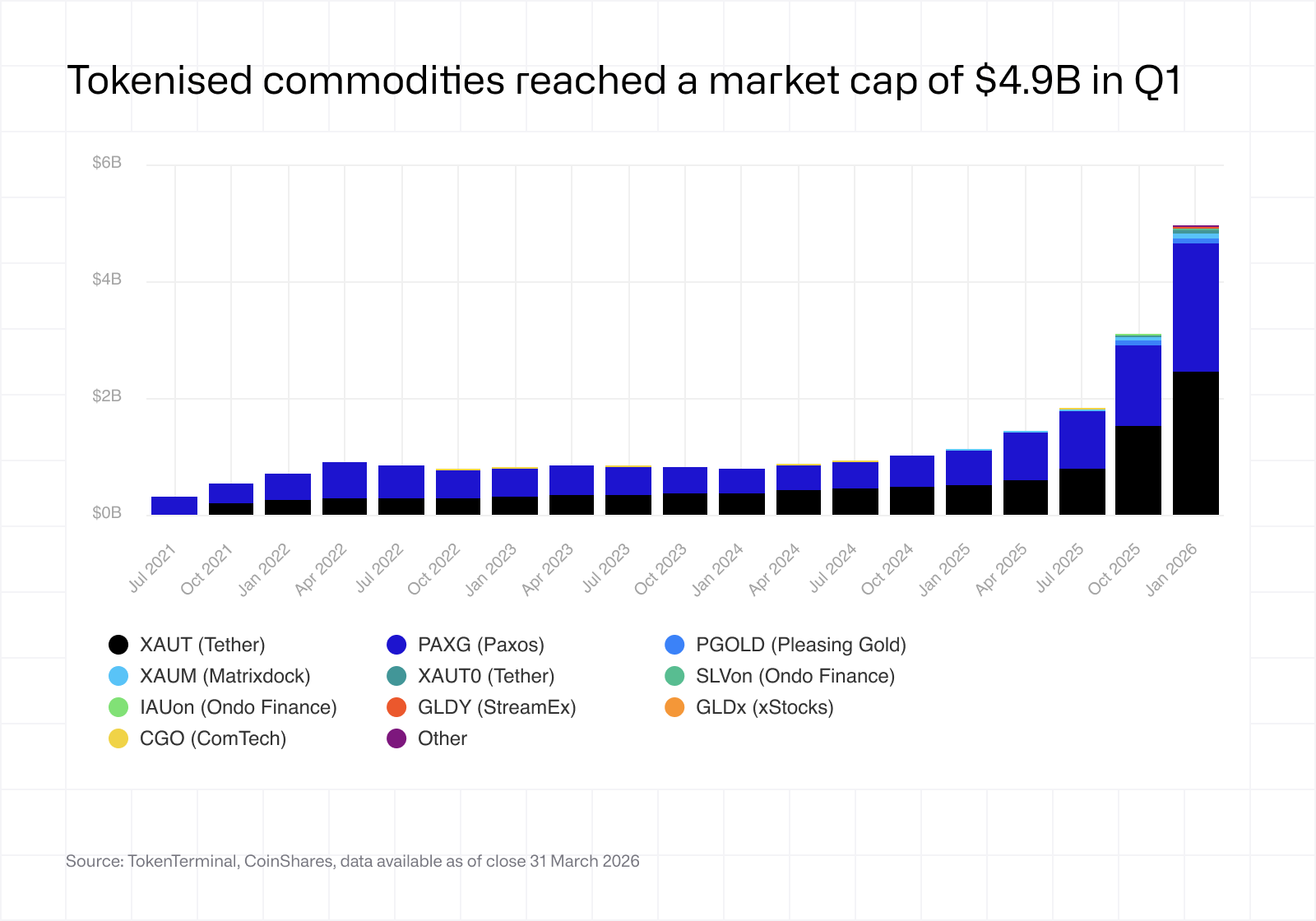

Matières premières tokenisées

Les matières premières tokenisées5 font entrer les actifs physiques sur la blockchain, ouvrant la voie à la propriété numérique et à la transférabilité à l'échelle mondiale.

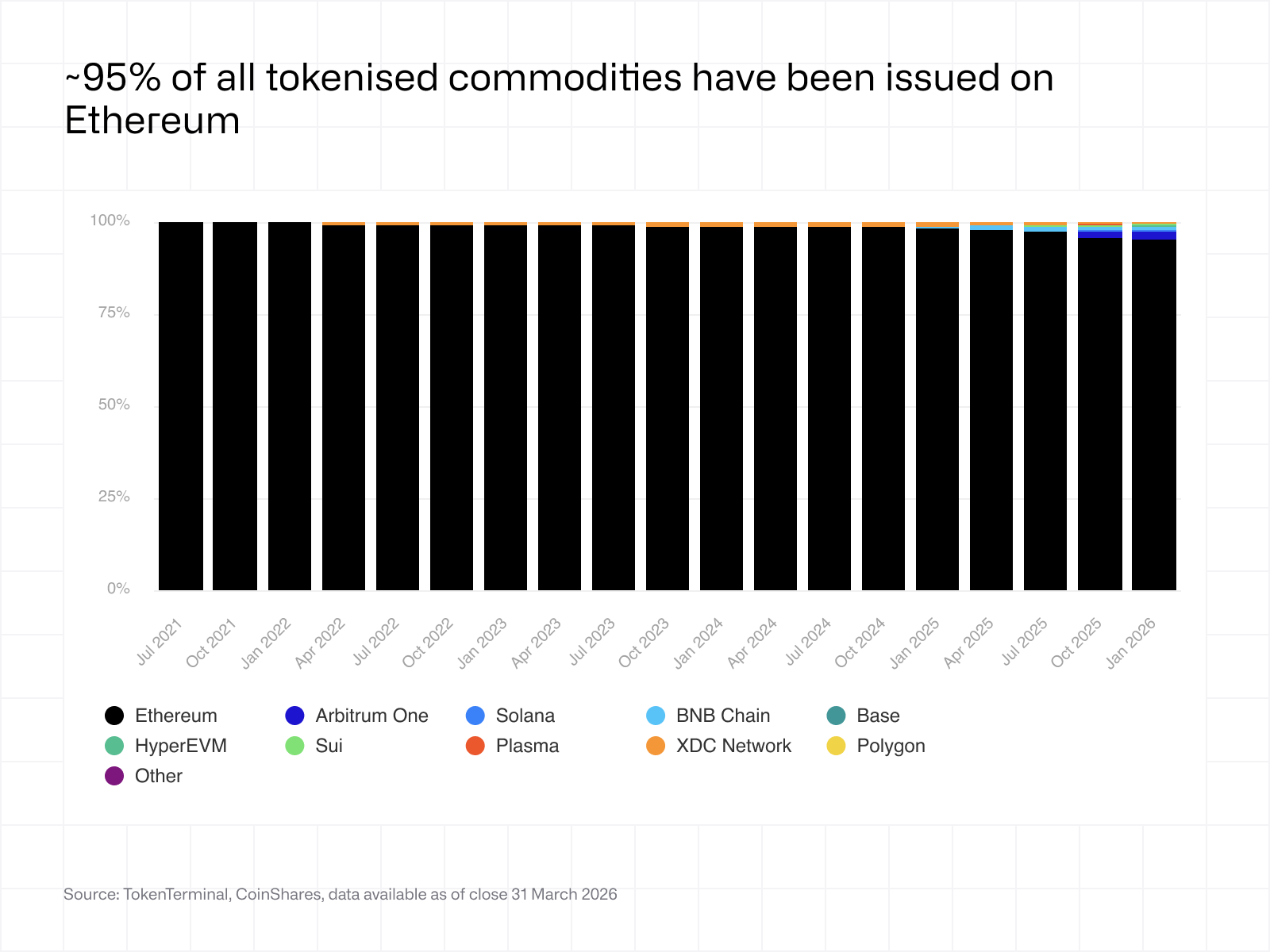

Ce segment connaît lui aussi une croissance soutenue. Au premier trimestre, les matières premières tokenisées ont atteint 4,9 milliards de dollars de capitalisation on-chain, contre 3,1 milliards au T4 2025 (+59,7 %), alors qu'elles restaient encore marginales il y a un an (1,1 milliard de dollars, soit +350 %). Les tokens adossés à l'or dominent la catégorie, traduisant une demande forte pour une exposition on-chain aux actifs traditionnels de réserve de valeur. Cette croissance est principalement portée par deux émetteurs : Tether et Paxos. XAUT ( le token or de Tether) et PAXG (celui de Paxos) ont tous deux enregistré une demande croissante ces derniers trimestres, portée par l'appréciation du cours de l'or. Environ 95 % des émissions de matières premières tokenisées sont concentrées sur Ethereum, ce qui en fait la couche de règlement la plus dominante de l'ensemble de la finance hybride.

Entreprises on-chain

Les entreprises on-chain représentent une nouvelle catégorie de sociétés natives d'internet qui génèrent des revenus directement à partir d'une activité sur blockchain et en redistribuent une partie à leurs détenteurs de tokens.

Au premier trimestre, les principales entreprises on-chain ont généré 587,9 millions de dollars de revenus, fortement concentrés parmi un petit nombre de plateformes de trading et d'émetteurs de stablecoins: Hyperliquid et Sky. Contrairement à Tether et Circle, une partie des revenus de Sky est native du protocole : elle provient des frais de stabilité facturés aux emprunteurs qui émettent des USDS contre du collatéral on-chain, ce qui lui vaut également de figurer dans cette catégorie. Sky alloue toutefois une part significative de la liquidité USDS vers des sources de rendement off-chain, faisant d'elle un cas intermédiaire, plus ancré on-chain que Tether et Circle, sans l'être entièrement.

Ces plateformes démontrent que les entreprises on-chain sont capables de générer des revenus substantiels fondés sur des commissions, ce qui rend leur profil économique comparable à celui des acteurs traditionnels des services financiers. Elles sont ainsi de plus en plus valorisées selon les cadres classiques des marchés cotés, notamment les multiples de revenus et de résultats.

Couches de règlement

Les blockchains L1 et L2 généralistes assurent le règlement de volumes importants d'actifs tokenisés, mais ne monétisent que l'activité transactionnelle, et non les actifs eux-mêmes. Leur modèle de revenus est fondé sur l'usage, ce qui signifie que les revenus progressent avec les transferts et les interactions, et non avec les encours ou les AUM. Il en résulte un écart structurel entre la valeur économique supportée et les revenus effectivement captés.

Les stablecoins l'illustrent clairement. Ethereum sécurise environ 180 milliards de dollars d'offre en stablecoins. À un rendement de 4 %, cela représente environ 7 milliards de dollars de revenus annuels pour les émetteurs. Ethereum n'en capte qu'une infime fraction via les frais de transaction, les utilisateurs payant par transfert et non pour détenir ou émettre l'actif. La valeur s'accumule du côté de l'émetteur, tandis que la couche de règlement reste économiquement sous-exposée au capital qu'elle supporte. Le chiffre plus modeste d'Hyperliquid s'explique par le fait que ses revenus proviennent de l'activité de trading et non des frais de règlement. Des précisions sont apportées dans la section suivante.

Conclusion

Les revenus et la valeur économique dans la finance hybride se distribuent selon un ordre bien précis : les entreprises on-chain en premier, puis les émetteurs d'actifs, et enfin les blockchains sous-jacentes.

Les entreprises on-chain comme Hyperliquid, Uniswap ou Aerodrome sont les premières bénéficiaires, car elles génèrent des revenus à partir du trading, de l'emprunt et de l'utilisation du collatéral. À mesure que davantage d'actifs réels migrent on-chain, ces plateformes accèdent à du collatéral porteur de rendement et adossé à des institutions, ce qui accroît les volumes de transactions et élargit leur base de revenus. Cette position devrait se renforcer au cours des 12 à 18 prochains mois, l'activité des utilisateurs continuant de se concentrer sur un petit nombre de plateformes offrant une liquidité profonde et des spreads serrés.

Les émetteurs d'actifs forment le deuxième niveau : ce sont eux qui émettent les actifs négociés, empruntés et utilisés comme collatéral. Dans les stablecoins, Tether et Circle s'imposent par leur distribution et leur liquidité, tandis que Sky et Ethena montent en puissance en proposant des alternatives génératrices de rendement. Dans les fonds tokenisés, BlackRock, Franklin Templeton et Ondo s'appuient sur leur crédibilité institutionnelle et leur accès aux rendements des bons du Trésor, un leadership qui devrait se maintenir, sauf si de nouveaux émetteurs améliorent leur distribution ou leur modèle économique. Dans les matières premières tokenisées, Tether Gold et Paxos Gold dominent, portés par la demande d'exposition à l'or, une situation qui devrait peu évoluer. Dans les actions tokenisées, Ondo et xStocks sont en tête, mais la catégorie reste ouverte en raison de sa taille encore modeste. Les positions dominantes pourraient évoluer rapidement à mesure que de nouveaux émetteurs entrent sur le marché et que la liquidité se développe.

Les blockchains constituent le dernier niveau, en monétisant l'activité transactionnelle générée au-dessus d'elles. Ethereum reste la couche de règlement dominante grâce à la profondeur de sa liquidité et à sa sécurité, tandis que les autres chaînes rivalisent sur les frais et le débit. Plus les actifs et les applications s'y concentrent, plus les volumes augmentent et plus les revenus de frais progressent. Hyperliquid illustre cette logique à sa manière. Sur les 12 à 18 prochains mois, la capacité des chaînes à attirer les principales applications et émetteurs sera déterminante, utilisateurs et transactions suivant naturellement là où la liquidité est la plus profonde.

À tous les niveaux, le mécanisme est identique : les actifs attirent la liquidité, les applications la transforment en revenus, les blockchains monétisent l'activité qui en découle. La question centrale est de savoir quelles applications et quels émetteurs s'imposeront comme choix par défaut, et quelles chaînes parviendront à fidéliser cette activité dans la durée.

Remarques finales

Hyperliquid: un exemple d’intégration verticale réussi

Hyperliquid capte de la valeur en combinant infrastructure et application au sein d'un système unique. Elle opère sa propre L1 tout en exploitant une plateforme décentralisée de produits dérivés qui génère l'essentiel de ses revenus. Cette approche déplace la monétisation des frais de règlement passifs vers des revenus directs au niveau des utilisateurs, là où les marges sont les plus élevées. Au T1 2026, Hyperliquid a généré 178,7 millions de dollars de revenus, dont environ 96 % provenant de l'activité de trading et une contribution minimale de la couche de base. En possédant l'application, Hyperliquid capte l'intégralité du flux économique de son cas d'usage principal, ses revenus progressant directement avec l'activité des utilisateurs.

Cela crée une pression stratégique pour les blockchains généralistes. Si la valeur continue de s'accumuler au niveau de la couche applicative, ces chaînes pourraient devoir monter dans la pile en lançant ou en intégrant des applications natives afin de capter des flux de revenus à plus forte marge. La contrepartie est structurelle : une plus grande captation des revenus se fait au prix d'une neutralité réduite et pourrait redéfinir l'organisation des écosystèmes.

1 Un stablecoin est un actif numérique conçu pour maintenir une valeur stable par rapport à une unité de référence, généralement le dollar américain, cette stabilité étant assurée par des mécanismes de collatéralisation, de gestion active ou de couverture.

2 Le USDS de Sky est traité ici en tant que stablecoin ; les mécanismes de son protocole générateurs de revenus sont abordés dans la section consacrée aux entreprises on-chain.

3 Un fonds tokenisé est un actif numérique représentant un capital d'investissement mutualisé, dont les décisions d'allocation sont exécutées par un gestionnaire désigné ou une stratégie programmable.

4 Une action tokenisée est un actif numérique représentant une participation dans une entreprise ou plusieurs entreprises, ou une exposition économique à celles-ci, cette exposition étant mise en œuvre par le biais de détentions d'actions directes ou de mécanismes synthétiques.

5 Une matière première tokenisée est un actif numérique représentant une propriété ou une exposition économique à des biens physiques, cette exposition étant mise en œuvre par le biais de détentions physiques ou de mécanismes synthétiques.

Publié leAvr 23rd, 2026