Ethereum 5-year valuation framework

![]() 27 Min. Lesezeit

27 Min. Lesezeit

- Ethereum

- Altcoins

We value ETH under a sum-of-parts framework combining cash-flow valuation (F1) and monetary premium valuation (F2) with a network/speculative overlay, projected across bear, base and bull scenarios over a five-year horizon. The headline outputs are as follows:

Bear: ~$1,443 implied price by 2031, a -9% annualised return from current spot.

Base: ~$4,935 implied price by 2031, a +16% annualised return.

Bull: ~$14,135 implied price by 2031, a +43% annualised return.

*See appendix for full model

1. Introduction

We have previously written an extensive framework by which we thought it was most logical to value ether. Ethereum changes quite frequently; network upgrades, monetary policy changes - these things force us to often change the way we view and value the network and underlying token. What is clear, at present, is that the market is struggling to price ether. After Dencun moved execution off the base layer, the cash flows that supported the prior bull case collapsed, even as on-chain activity reached record highs. Weekly fees that peaked above US$200m in early 2024 now run closer to US$10m, while monthly active users have roughly doubled over the same period.

There are conflicting views being expressed around the crypto-sphere. Some say that with the fee story gone, the implied value of the ether token has gone with it, whilst others argue that the token has evolved to represent a type of money, warranting a premium that should grow with the ecosystem it secures. Both views are partially correct, and neither alone produces a defensible number.

This report sets out a sum-of-parts framework that seeks to value ether as a mixture of both. The first framework treats the network as a business, projecting fee revenue across the major usage categories and applying a multiple. The second framework treats ether as the money and collateral base of the largest smart contract ecosystem, sizing the annual demand from staking, DeFi, layer-2 reserves, ETFs, corporate treasuries, and store-of-value buying. A network and speculative premium sits on top of the second component, capturing the value that accrues to ether from securing a growing on-chain economy and the cyclical sentiment that drives prices far above fair value in bull markets, and far below fair value in bear markets.

Ether is not a tech stock and it is not digital gold. It is the native asset of a permissionless platform on which builders can deploy essentially anything, drawing on decentralised security, leading liquidity, and global access. Within that ecosystem, ether also functions as money and as collateral.

The output is a 5-year projection of ether's price under bear, base, and bull scenarios, accompanied by the full model assumptions. One note worth flagging up front: rather than deriving ether's fair value from zero, we anchor Framework 2 to today's market cap and project the path forward from there. The alternative, pricing the monetary premium from zero, requires assumptions about how much of global gold, M2, or smart contract TAM ether "should" capture, and we don't think any of those numbers can be defended with any real conviction today.

The market is currently pricing ether at ~US$260-284B. We aren't claiming that's correct. We're claiming it reflects where buyers and sellers have agreed given all the visible information: post-Dencun fees, current staking ratios, ETF flows, competitive positioning, and speculation. The model decomposes that figure into a cash-flow component (Framework 1) and a residual monetary component (Framework 2), then projects forward. The report answers where ether's price could go over five years, not whether it is mispriced today. The consequences of this choice are discussed in the limitations section.

2. Ethereum has changed... A lot

Ether's monetary policy has changed more than any other major digital asset. Between 2015 and 2022, the network operated on proof-of-work with average annual issuance of ~4.5%. The Merge in September 2022 transitioned Ethereum to proof-of-stake and cut issuance by over 90%.

EIP-1559, a highly impactful network change, was implemented in August 2021, restructuring the fee market so that the base fee of every transaction is permanently burned, or removed from circulating supply, rather than paid to validators. The economic effect is similar to that of a share buyback, with the network using its revenue to retire supply on behalf of all holders. Validators retain priority tips and any value extracted from MEV. 80-95% of fee revenue currently accrues to the burn, with 5-20% flowing to validators.

This combination of low issuance and burn gave ether its popular "ultrasound money" narrative. Fee revenue was high enough post-merge that burn frequently exceeded issuance and supply contracted in absolute terms. Valuing ether based on its fee revenue was straightforward and logical. Usage translated to revenue, which translated to value accrual to token holders.

The Dencun upgrade in March 2024 broke that alignment. Dencun introduced blob transactions, a dedicated data availability lane that allowed layer-2 networks to post compressed transaction data to Ethereum at a fraction of the previous cost. Execution moved off the base layer dramatically. Layer-2 throughput expanded sharply, user-facing transaction costs collapsed, and the fee revenue that had supported ether's cash-flow story fell by an order of magnitude. Our analysis of the Dencun upgrade covers the mechanics in more detail. The summary version is that Ethereum chose to scale by outsourcing execution to L2s, and the immediate consequence was a large decline in L1 fee revenue. As seen in the chart above, fee revenues fell dramatically and ether struggled to maintain its ultrasound money narrative.

The Dencun upgrade in March 2024 broke that alignment. Dencun introduced blob transactions, a dedicated data availability lane that allowed layer-2 networks to post compressed transaction data to Ethereum at a fraction of the previous cost. Execution moved off the base layer dramatically. Layer-2 throughput expanded sharply, user-facing transaction costs collapsed, and the fee revenue that had supported ether's cash-flow story fell by an order of magnitude. Our analysis of the Dencun upgrade covers the mechanics in more detail. The summary version is that Ethereum chose to scale by outsourcing execution to L2s, and the immediate consequence was a large decline in L1 fee revenue. As seen in the chart above, fee revenues fell dramatically and ether struggled to maintain its ultrasound money narrative.

If you were to take a purely cash-flow based valuation for ether, it would say the token is dramatically overvalued. Conversely, if you did a rough TAM analysis on digital gold, or estimates on how much value the Ethereum network will secure in 3, 5 or 10 years, you would likely come to the conclusion that the token is dramatically undervalued. The reason why a hybrid approach is necessary in light of the changes made to the network, is that usage has never been higher:

The amount of ETH bridged to L2’s is near all time highs

The amount of active users on L2’s is at all time highs

The amount of active users on the main chain is at all time highs

It would be disingenuous to say that Ethereum has failed. It hasn’t - It is clearly driving enough utility that more and more users are choosing to transact on both the main chain and on layer 2s.

The analysis therefore combines three components. The first treats Ethereum as a business and asks what its fee revenue is worth, projected over five years across eight activity categories. The second treats ether as a monetary and collateral asset, sizing the annual demand from six sources: staking, DeFi, layer-2 reserves, ETFs, corporate treasuries, and store-of-value buying. The third is a premium overlay applied to the second, capturing network effects on one hand and the cyclical sentiment that swings prices above or below fair value on the other. Together, these three components produce an implied price for the token over 5 years under different scenarios.

3. Framework 1: Ether as a cash-flow asset

Ethereum is a network that sells blockspace. Users pay fees to transact, and under EIP-1559 those fees split two ways. The base fee, which accounts for 80-95% of total fee revenue (market activity dependent), is permanently destroyed. The remainder, consisting of priority tips and value extracted from transaction ordering (MEV), flows to validators. The burn is economically similar to a share buyback, removing supply on behalf of every ether holder, and it is the primary mechanism through which network usage accrues to the token.

If Ethereum is treated as a business and its blockspace as a product, the question becomes straightforward: what is the present value of the revenue that blockspace will generate, and what does that imply for fair value? Fees are denominated in US$ throughout the model to avoid circularity with the ether price itself.

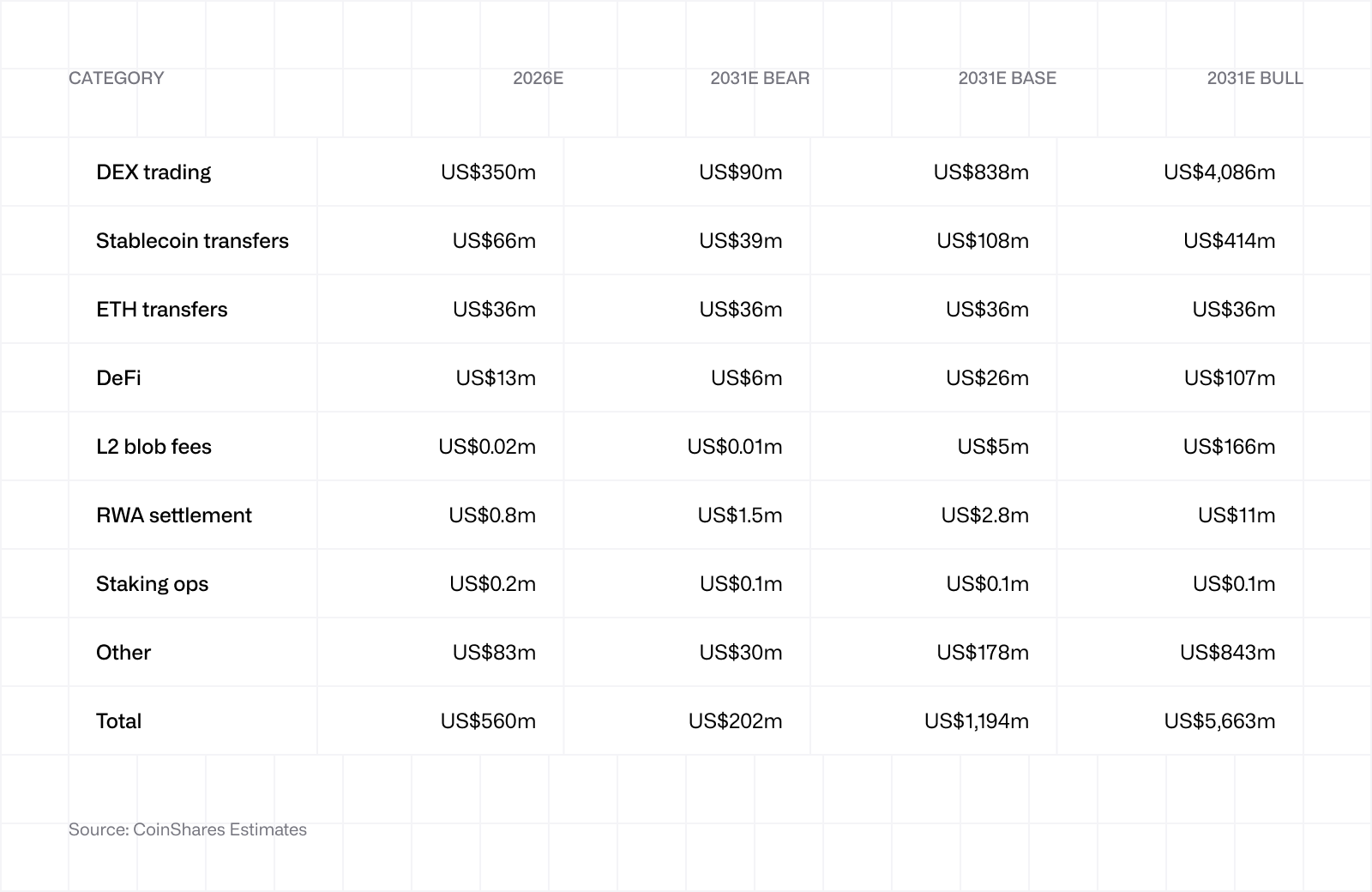

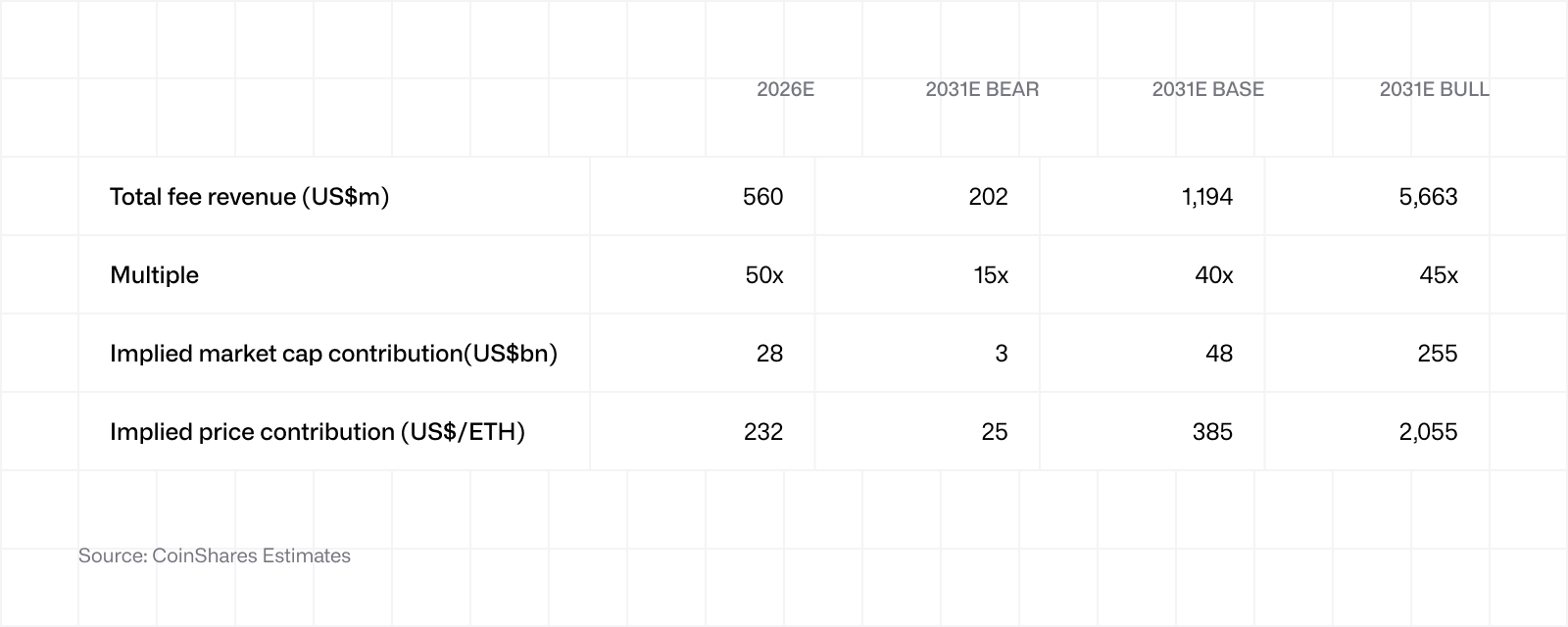

The model projects fee revenue across eight categories over a 5-year horizon. The four largest by potential contribution are DEX trading, stablecoin transfers, DeFi activity (ex-DEX), and layer-2 data posting via blob transactions. The remaining four (ether transfers, real-world asset settlement, staking operations, and a residual "other" bucket) are smaller and mostly negligible for the overall fee revenues. (n.b. Layer-2 data posting is also negligible but in our view highly likely to have some form of modification via network upgrades over time).

The full set of category-level assumptions and outputs is shown below.

DEX trading is the single largest contributor in the base case and the category most exposed to share loss. Solana and other alt-L1s have taken DEX market share over the past 18 months, and Base/Arbitrum et al. settle to Ethereum without contributing directly to L1 fee revenue. The base case holds L1 share flat at 20% on the view that liquidity stickiness, institutional preference for Ethereum settlement, and the deepening of on-chain order books for tokenised assets prevent further erosion. The bear case allows share to drift to 11%, the bull case has it expanding to 35% as institutional flows concentrate on Ethereum settlement.

Stablecoin transfers are the second-largest contributor. Ethereum currently hosts ~52%2 of total stablecoin supply, above US$300B in circulation. The model holds this share constant across the base case while the underlying market compounds at 20% to reach US$870B by 2031, with Ethereum's share producing ~US$450B on chain. The GENIUS Act is treated as a 2026 tailwind. Per-transfer fees compress from US$0.20 in 2026 to US$0.08 by 2031, reflecting the throughput improvements discussed below.

Layer-2 blob fees remain small across all scenarios. This is intentional rather than an oversight. Blob fee revenue depends on a moving target, with the network periodically increasing blob capacity (currently 14 per block, projected to reach 24 by 2031) and per-blob fees remaining a function of demand against an aggressively expanding ceiling. The model treats layer-2 value as accruing to ether through the network premium discussed later, where additional L2 economic activity flows through to ether's role as the settlement and collateral base, rather than through direct fees. Blob mechanics overall may evolve differently than assumed due to network upgrades.

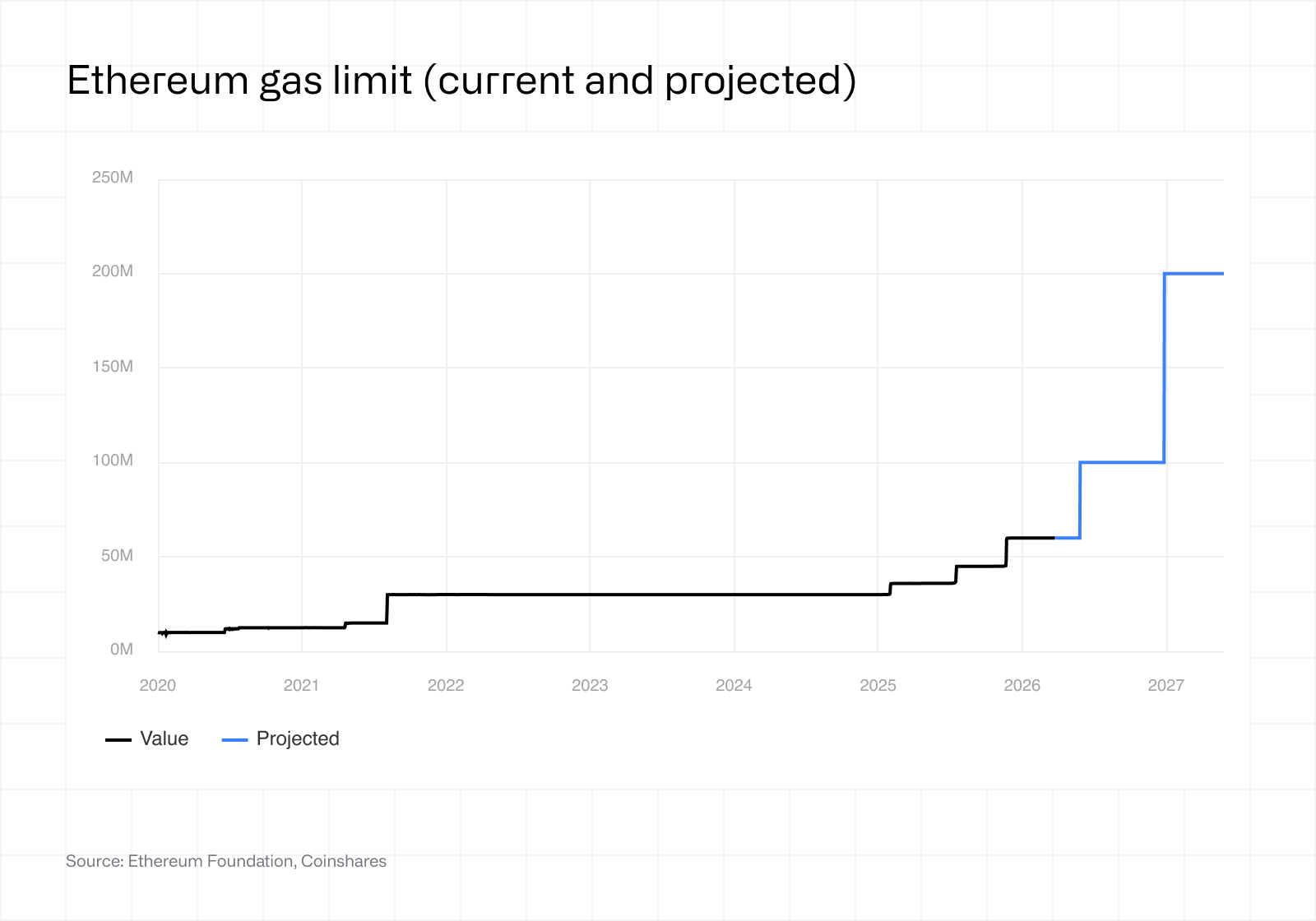

Within our projections, we have taken current and future network changes carefully into account. Ethereum's gas limit (simple terms: amount of transactions per block) doubled from 30M to 60M over the past year, the first significant increase since 2021. The Glamsterdam upgrade, currently scheduled for Q3 2026, is expected to take the gas limit to 200M, a 3.3x increase alongside parallel execution and enshrined proposer-builder separation.

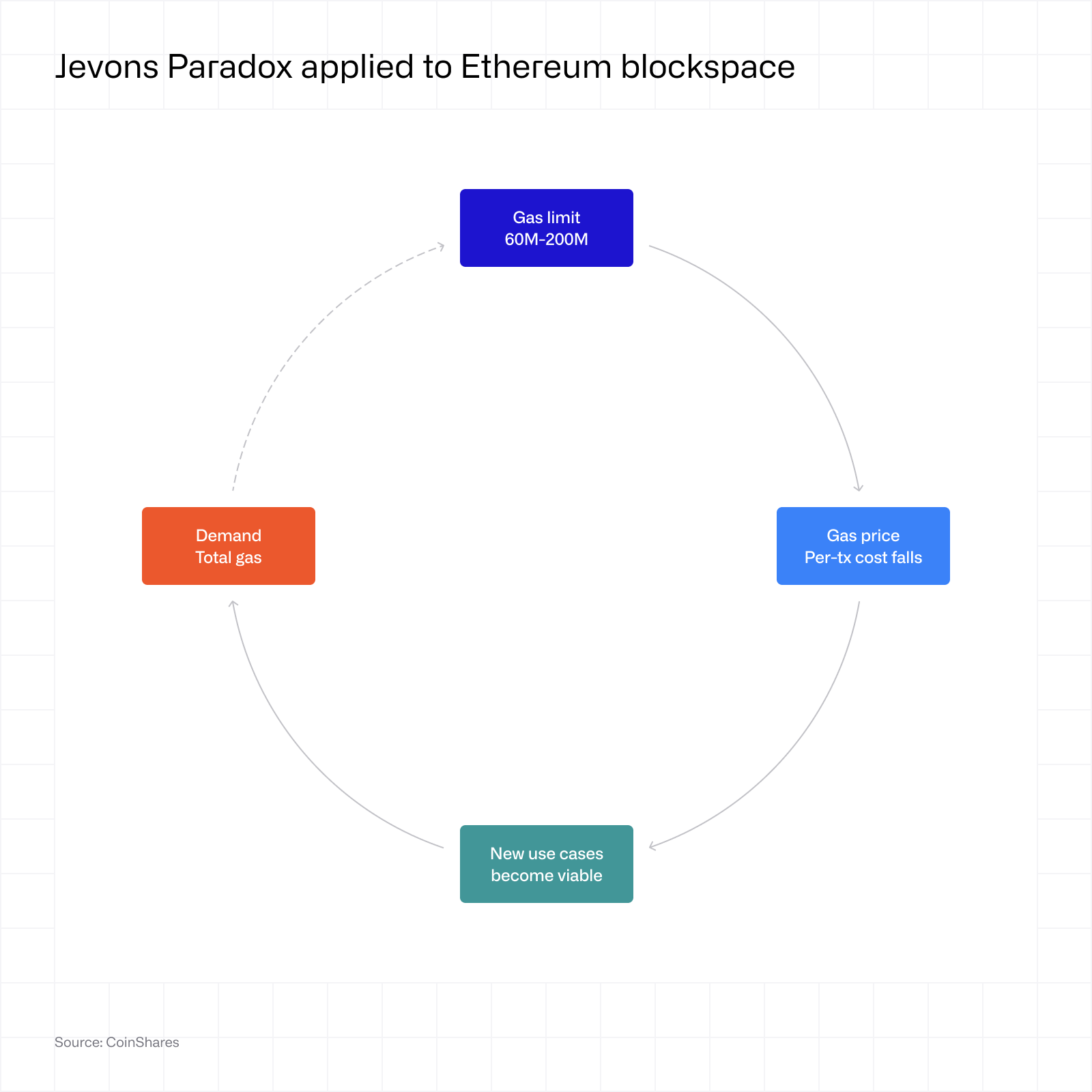

This is where Jevons paradox comes in. The term describes a counterintuitive phenomenon: when the cost of using a resource falls, total consumption often rises by enough that aggregate usage grows rather than shrinks. The term is thrown around by Ethereum researchers frequently, and it captures the long-term ambition for the network. Make individual transactions dramatically cheaper, expand throughput by an order of magnitude, and let the wave of new activity grow total fee revenue even as fees per user fall. The bull case for ether's cash flows depends on this playing out. If demand fails to expand fast enough to offset cheaper transactions, the network ends up busier and less profitable at the same time.

This is where Jevons paradox comes in. The term describes a counterintuitive phenomenon: when the cost of using a resource falls, total consumption often rises by enough that aggregate usage grows rather than shrinks. The term is thrown around by Ethereum researchers frequently, and it captures the long-term ambition for the network. Make individual transactions dramatically cheaper, expand throughput by an order of magnitude, and let the wave of new activity grow total fee revenue even as fees per user fall. The bull case for ether's cash flows depends on this playing out. If demand fails to expand fast enough to offset cheaper transactions, the network ends up busier and less profitable at the same time.

A multiple is applied to projected fee revenue to derive an implied market cap contribution. Base case uses 50x on 2026 fees moving down to 40x by 2031, bear case goes from 20x to 15x, bull has 70x then dropping over time to 45x. The 40-50x range is high by mature standards but consistent with early-stage profitable tech businesses growing fees at 15-20% CAGRs. The model in the appendix shows the base case is equivalent to a 12% required return over five years, or 48x on 2026 fees once discounted back.

A multiple is applied to projected fee revenue to derive an implied market cap contribution. Base case uses 50x on 2026 fees moving down to 40x by 2031, bear case goes from 20x to 15x, bull has 70x then dropping over time to 45x. The 40-50x range is high by mature standards but consistent with early-stage profitable tech businesses growing fees at 15-20% CAGRs. The model in the appendix shows the base case is equivalent to a 12% required return over five years, or 48x on 2026 fees once discounted back.

Framework 1 produces an implied ether price contribution ranging from US$25 in the 2031 bear case to US$2,055 in the 2031 bull case, with the base case at US$385. These are the cash-flow contributions to the total.

4. Framework 2: Ether as a monetary and collateral asset

A pure cash-flow valuation captures what users pay to transact, but it does not capture what they hold the asset for, or why. Ether is the native asset of an economic system that secures hundreds of billions of dollars in tokenised value. It is required to pay for every transaction on the network. It is the primary collateral in DeFi lending markets. It is the reserve asset held by nearly every layer-2 sequencer and bridge. It underpins the most active stablecoin economy, with ether-settled stablecoins accounting for over half of total stablecoin supply globally. None of this value accrues through fee revenue, and none of it is captured by Framework 1.

This is the monetary premium. The value ether commands beyond its cash flows, derived from its role as the collateral and settlement currency of the largest smart contract ecosystem. Framework 2 estimates this premium and projects how it evolves over a 5-year horizon.

The model identifies six structural demand sources. The first three reflect ether locked into specific functions: staking (currently around 39m3 ether deposited with validators), DeFi collateral (ether deployed as backing for lending and liquidity positions), and layer-2 reserves (ether held by L2 sequencers, bridges, and treasuries). The remaining three are flow-based, denominated directly in dollars: ETF net flows, corporate treasury buying, and store-of-value buying from passive holders.

For the locked sources, the year-on-year change in ether held is multiplied by spot price to derive dollar buying pressure, with spot fixed at US$2,350. The six sources are summed into net annual buying pressure.

Net buying pressure is then translated into market capitalisation impact via a regime multiplier, which captures the price elasticity of net buying against the orderbook. The multiplier is 0.7x in the bear case, where buying is absorbed easily against willing sellers. It is 1.5x in the base case, reflecting a standard market cap uplift of US$1.5 per US$1 invested. It is 3x in the bull case, where there tends to be fewer willing sellers, more positive price discovery, and buying pressure is amplified.

These multipliers are deliberately conservative against academic literature. Garratt and van Oordt's crypto multiplier model (BIS, 2023)4 puts the floor for market-cap response per US$1 of net inflow at

M/(M-Z),

where Z is the supply held as a store of value rather than a transactional float. With ~60% of ETH sitting in either smart contracts or in inactive addresses (>6 months), the implied lower bound for ether is ~2.5x. Our bull case at 3x sits just above this figure. Our base at 1.5x and bear case at 0.7x sit well below it. We therefore think the multiples chosen for each scenario are defensible and somewhat conservative.

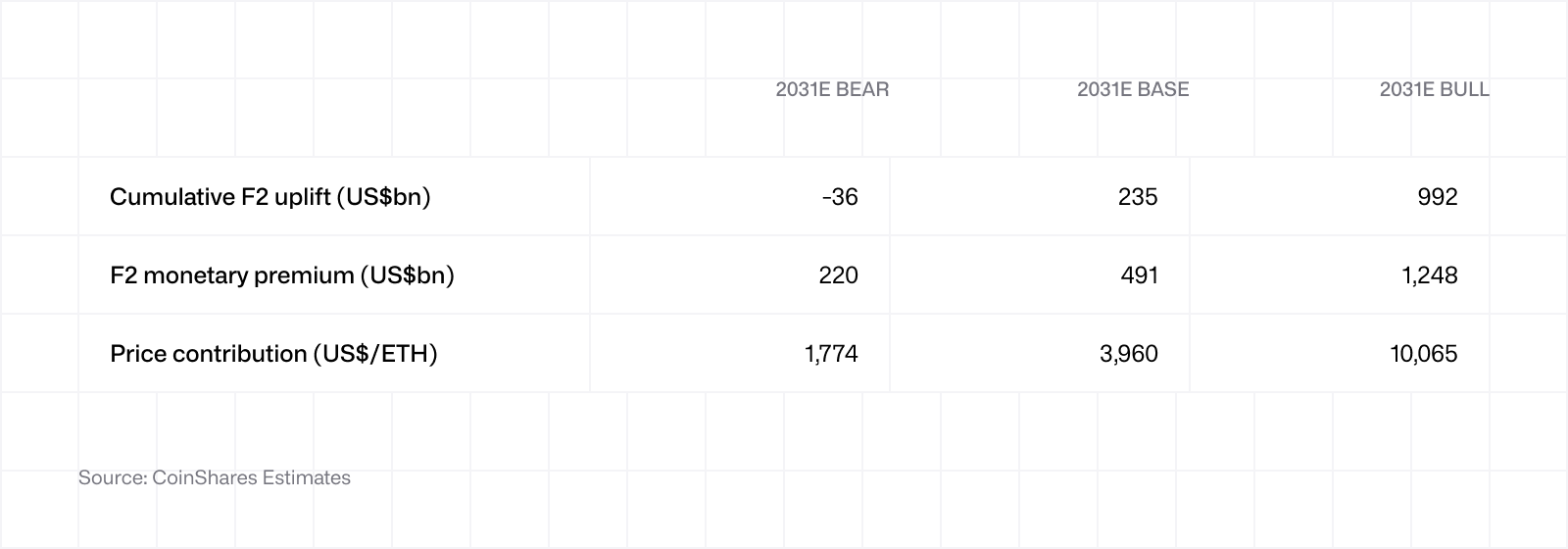

Annual market cap uplifts are summed across the forecast, then added to a baseline calculated as current observed market cap (~US$284B) minus the Framework 1 base case 2026 market cap (US$28B), giving US$256B. This ultimately means that our valuation is taking into account that the current price on the screen is a decomposition of a variety of factors, and our framework seeks to project the path from here.

Framework 2 produces a 2031 implied price contribution ranging from US$1,774 in the bear case to US$10,065 in the bull case, with the base case at US$3,960. This is a wider distribution than Framework 1 produces, reflecting the fact that there is ultimately a very wide distribution of potential states the network could be in 5 years down the line.

Framework 2 produces a 2031 implied price contribution ranging from US$1,774 in the bear case to US$10,065 in the bull case, with the base case at US$3,960. This is a wider distribution than Framework 1 produces, reflecting the fact that there is ultimately a very wide distribution of potential states the network could be in 5 years down the line.

5. Putting it together

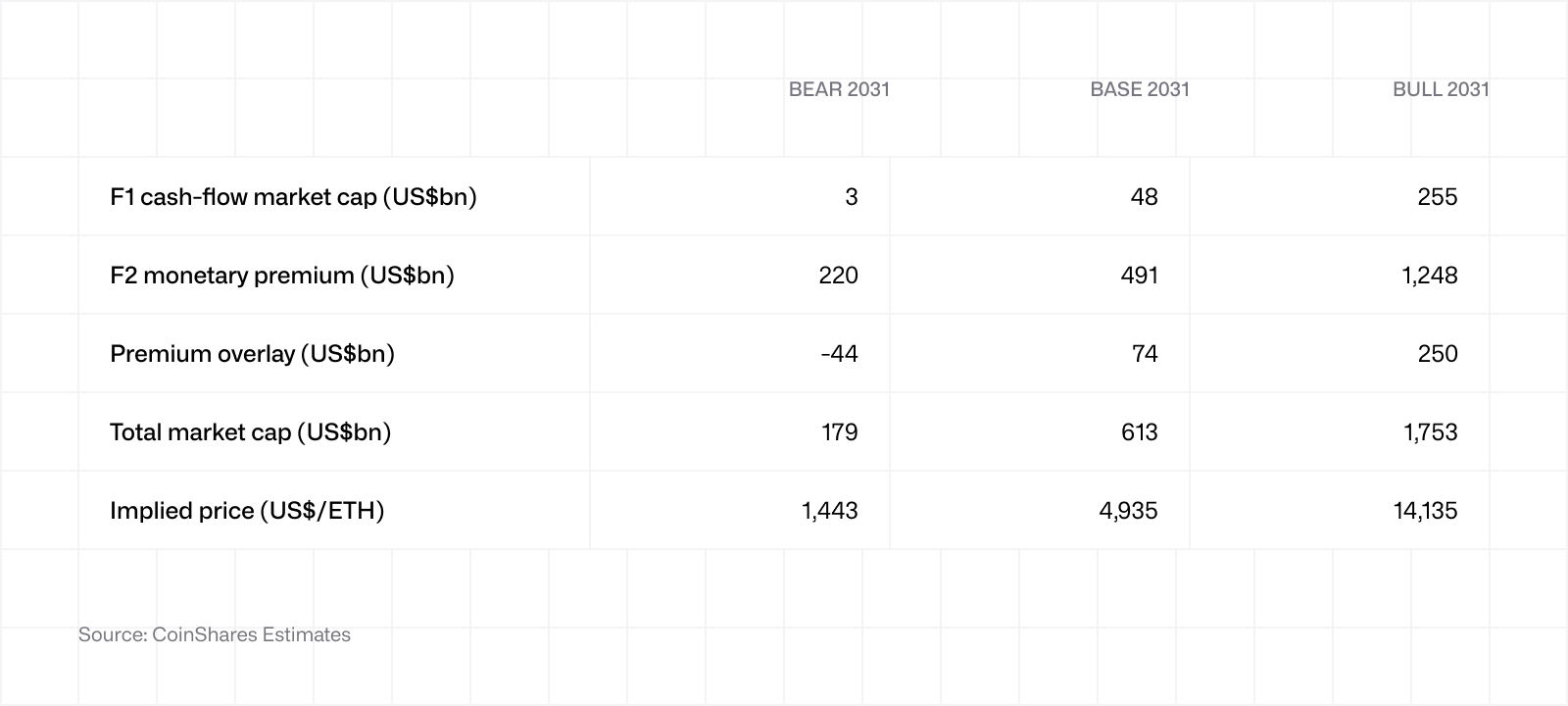

The three components sum additively into a total market cap, which is then divided by projected supply to give an implied price for the ether token. The formula is:

Total = (F1 market cap + F2 × (1 + premium)) ÷ projected supply (122-124m)

The cash-flow value of fee revenue in Framework 1 is already captured by the multiple applied in section 3, so applying a premium on top would double-count. The premium overlay applies only to Framework 2. The same dollar of recurring buying will command a premium or a discount depending on Ethereum's position within the smart contract platform market.

The premium overlay has two components:

Network value: the structural premium ether commands as the security and settlement layer of a growing on-chain economy.

Speculation: the cyclical sentiment that drives prices far above fair value in bull markets, and far below fair value in bear markets.

Premium percentage by scenario:

Base case: 12% in 2026, stepping up to 15% from 2027 onwards.

Bull case: 20% throughout, reflecting the elevated premium ether has historically commanded in bull markets

Bear case: negative, from -5% in 2026 to -20% by 2031. (Ethereum has failed/crypto has failed)

Composition of the overlay over time. The split between network value and speculation shifts as the network matures. In 2026, the overlay is weighted toward speculation, reflecting current market positioning where sentiment dominates fundamentals. By 2031, network value grows as a share of the premium on the view that perceived riskiness falls and network effects compound at larger ecosystem size.

Base case: network value rises from 25% of the overlay in 2026 to 60% by 2031.

Bull case: network value reaches 80% of the overlay by 2031.

Combining the three components produces the headline output of the framework. The 2031 implied market caps and implied prices are shown below.

The three components are not equal contributors. Across all scenarios, Framework 2 is the largest single driver of the total, reflecting the model's view that the monetary premium is the dominant source of ether's value.

The three components are not equal contributors. Across all scenarios, Framework 2 is the largest single driver of the total, reflecting the model's view that the monetary premium is the dominant source of ether's value.

6. Scenarios and outputs

Bear case (US$1,443 by 2031)

The bear case is a scenario in which Ethereum loses its position, either to competing layer-1 blockchains or because the broader thesis for crypto as a productive asset class has not played out. Fee revenue declines from current run-rates rather than recovering, with DEX market share contracting to 11% as alternative venues capture attention and volumes. Stablecoin share actually remains competitive at 40%, but overall stablecoins growth doesn’t materialize, and the market stays somewhat stagnant.

The structural demand sources turn negative across the board. Staking declines as validators exit, DeFi collateral contracts, layer-2 reserves shrink, ETF flows remain in sustained outflow toward zero, and corporate treasuries become net sellers as digital asset treasury companies unwind balance sheet positions. The premium overlay actually becomes a discount.

Risks embedded in this scenario include regulatory friction under frameworks such as the CLARITY Act that favour intermediated structures over permissionless DeFi, sustained competitive pressure from higher-throughput chains, and longer-tail risks including quantum computing developments that affect assumptions across the digital asset space, although these latter risks apply broadly rather than to Ethereum specifically.

Base case (US$4,935 by 2031, 16% CAGR)

The base case is a scenario where the current growth drivers for Ethereum continue at modest paces, and that Ethereum remains the dominant smart contract blockchain. DEX volumes grow at a 17% CAGR with market share held flat at 20%. Stablecoin supply on Ethereum reaches ~US$450B by 2031, consistent with the GENIUS Act tailwind and historical growth rates. DeFi TVL compounds at 25% (although an argument could be made that recent DeFi exploits threaten this ability), RWA tokenisation builds steadily, and layer-2 activity is accretive through an increase in bridged/stationary ETH.

ETF inflows build to US$25B annually by 2031, corporate treasury allocations increase gradually, and store-of-value buying grows as the asset class matures. Here we apply a 12-15% premium on the network as Ethereum delivers on its forecasted growth rates and gets rewarded by the market, with some speculative fervour. Implied upside to current spot is ~110% over five years, equivalent to a 16% annualised return.

Bull case (US$14,135 by 2031, 43% CAGR)

The bull case requires the six demand catalysts identified in section 4 to compound at high levels, with Ethereum increasing its market share over time as opposed to maintaining it. Fee revenue reaches US$5.7B by 2031, supported by DEX volumes growing at a 25% CAGR through 2031 with L1 share expanding to 35% (with per-user fees decreasing substantially). Stablecoin supply reaches US$2.8T at a 50% CAGR, fulfilling Scott Bessent’s optimism consistent with bull-case GENIUS Act adoption, and RWA tokenisation scaling to US$420B on Ethereum specifically. One might consider this scenario an “everything has worked out perfectly and more” scenario.

The structural demand sources remain at elevated levels with ETF flows reaching US$40B annually, corporate buying scaling to US$25B, and store-of-value demand building meaningfully. The regime multiplier of 3x reflects a lack of willing sellers in what would be described as a multi-year bull market of a network growing into the most optimistic forecasts. The premium overlay becomes less speculative over time and more so attributed to the established network effects as Ethereum becomes the venue for finance on-chain. Implied upside to the current spot price is ~500%, equivalent to a 43% annualised return.

7. Conclusion

We assign the highest probability to somewhere between the base and bull case. Ethereum doesn't need to win every category to clear US$4,935 by 2031. It needs to hold DEX share roughly where it is, keep its stablecoin position, deliver scaling upgrades (Glamsterdam first, then others), and have ETF flows pick up to match bitcoin on a market cap adjusted level. None of that requires any crazy assumptions, and it may very well be that these prove far too conservative. The bull case requires more things to go right than we are willing to say with confidence today, and the bear case requires our assumptions to go wrong across the board, whether through a competing ecosystem displacing Ethereum or crypto infrastructure failing more broadly.

Ether is neither a tech stock nor digital gold, and any framework that treats it as only one will, in our view, not capture the entirety of the value proposition. The market's current confusion about how to price ether reflects this. After Dencun, fees dropped but overall usage of the network has continued to increase, reflected in mainnet activity and Layer 2 TPS.

This is one way to value ether, not the only way. Other frameworks are equally defensible and bring different lenses to the network and the token. It is not an easy task, and if it was, there would be a universally accepted methodology.

What these two frameworks seek to do is encapsulate what we believe is a multi-faceted asset, one that changes over time (sometimes for the better, sometimes for the worse) and that is moulding into an endgame which is not yet clear, but is becoming clearer. For now, that endgame looks something like this: scale the main chain as aggressively as possible without compromising on security or decentralisation, drive transaction costs low enough that finance can move on-chain at scale, and keep ether at the centre of it as the asset that secures and settles the whole system.

Limitations

Framework 2 is anchored to the current market cap, not derived from zero. The US$256B baseline is calculated as today's observed market cap minus Framework 1's base case 2026 value. The model is therefore a 5-year path projection conditioned on current positioning, not a fair-value estimate today. Someone looking for a clean answer to "is ether undervalued today" will only find a partial one here.

The regime multiplier is a large contributor in Framework 2:

Base case at 1.0x rather than 1.5x reduces the 2031 base implied price by ~15%.

Bull case at 2x rather than 3x reduces the 2031 bull implied price by ~23%.

The multipliers seek to put a conservative estimate on how price amplification is varied, depending on the type of market regime we are in.

Framework 1's 40-50x multiple is defensible but not riskless. The appendix shows the calibration is consistent with a 12% required return over five years, equivalent to early-stage profitable tech. If the market applies a mature infrastructure multiple instead (10-15x), Framework 1's contribution compresses very significantly.

Layer-2 economics remain a structural uncertainty. The model assumes blob fees stay small and that L2 value accrues through the Framework 2 network premium rather than direct fees in Framework 1. This is reasonable given current network parameters, but blob pricing could easily be modified in the future. If post-Glamsterdam blob economics shift materially, it is likely that a big part of this methodology would have to be revisited.

What we will be watching

Fee revenue trajectory through 2027. The current run-rate is depressed relative to history. The base case requires recovery as activity scales post-Glamsterdam.

ETF flows. Currently weak and a central figure in our projected demand for base and bull cases in Framework 2.

Gas limit milestones. Glamsterdam in Q3 2026 could push the gas limit to 200m. Further changes could happen quicker or slower. We have modelled transaction fees for individual categories and number of transactions based on assumptions. These assumptions might have to change.

Monetary policy changes. Any further adjustment to issuance, burn mechanics, or validator economics would alter the supply path

Blob mechanics. The model assumes blob fees stay small. A change in blob pricing policy or capacity expansion schedule would force a revisit of Framework 1's L2 assumptions.

Hard forks. Major protocol changes outside the scheduled upgrade roadmap (security patches, contentious EIPs, governance-led shifts) introduce uncertainty across the model as a whole.

Quantum hardening. Should research priorities pivot toward quantum-resistant cryptography, scaling work could slow. This is a low-probability concern in our 5-year window, but a real one over longer horizons.