What is Open USD (OUSD) and what does it mean for stablecoins?

![]() 6 min read

6 min read

The materials on this website or any third-party websites accessed herein are not associated with and have not been reviewed or approved by: (i) Valkyrie Funds LLC dba CoinShares, its products, or the distributor of its products, or (ii) CoinShares Co., its products, or the marketing agent of its products.

Executive summary

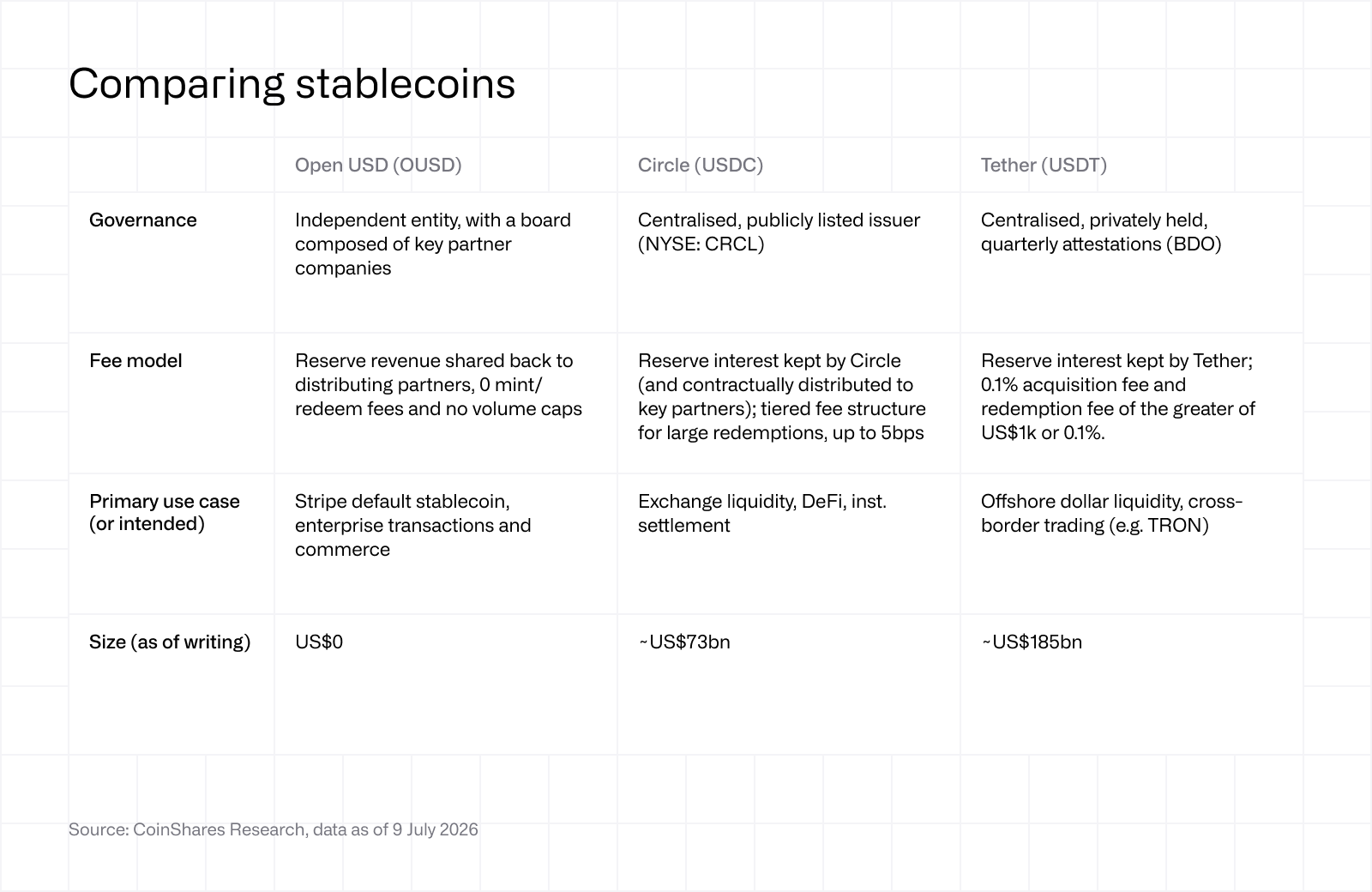

Open USD (OUSD) is a new stablecoin from Open Standard, backed by 140+ partners including Visa, Mastercard, Stripe, BlackRock and Coinbase. Launch is expected in H2 2026.

Its model shares reserve income with the partners that distribute it, minus a management fee, rather than the issuer keeping it. Minting and redemption are free with no volume caps.

Key details remain unconfirmed: reserve composition, custodian, the management fee, and the full chain list.

Circle (USDC) fell upon announcement, and there are diverging opinions on how this stablecoin and model could threaten its moat.

Introduction

Open USD is a new stablecoin governed and operated by Open Standard, designed less as a retail crypto product and more as shared payments infrastructure for large businesses. The pitch is straightforward: companies can mint and redeem at scale with no fees or artificial volume limits, while also receiving the economic benefit from the reserves backing the stablecoin (partners receive the reserve yield instead of giving it all to the issuer), minus a small management fee. That is the main difference versus the existing stablecoin model, where the issuer keeps the reserve income (barring contractual distributions to partners, e.g. Coinbase-Circle).

The design goal here is to seek alignment. Open USD is trying to become the neutral stablecoin rail for payments companies, banks, fintechs, crypto firms and merchants, rather than a stablecoin controlled by a single issuer. The partner list spans over 140 businesses, including BlackRock, Coinbase, Mastercard, Stripe, and Visa.

If successful, Open USD could push stablecoins further into mainstream payments by making the economics and governance more attractive for the businesses actually using them.

The project is aiming to go live in H2 2026, with material details still unconfirmed: reserve composition, custodian, the management fee, and chains beyond Solana and Tempo, which have said OUSD will be issued natively on day one.

When compared to the stablecoin leaders, USDT (Tether) and USDC (Circle), there are some key differences in approach:

OUSD changes the stablecoin model by sharing reserve economics

Circle fell ~17.5% on 30 June, the day Open USD was announced, although the same week’s Russell reconstitution likely added technical pressure through passive selling. On the surface, the reaction looks obvious: Open USD lines up a 140-member consortium with hundreds of millions of combined users, and gives every one of them strong incentives to push it. Each keeps the interest on the reserves they help fund through minting.

This initially reads bearish for two reasons:

First, Circle is already fighting to grow USDC supply against an expanding list of new issuers, and OUSD has the potential to be the biggest of them by distribution. Worse yet, the margin it is actively trying to maintain is dependent on rates, which are hard to predict from here. Circle's economics largely track Treasury yields (and outstanding supply), which is why Q1 revenue of $694m came in below the prior quarter's $770m even as volume climbed.

Second, Circle already buys distribution by paying Coinbase roughly half of USDC's reserve income. OUSD takes that discretionary cost and makes it the default: every partner earns the yield. This could significantly alter what Circle’s partners can credibly demand.

The Circle–Coinbase revenue-sharing agreement reaches the end of its initial three-year term on 18 August 2026, only weeks after Coinbase joined the Open USD consortium. The deal does not simply lapse: if both parties have met their obligations and cannot agree on modifications, it automatically renews for another three years. That makes outright non-renewal unlikely, but it does give Coinbase a more credible negotiating position. It now has exposure to both sides of the stablecoin economics debate: USDC through its existing revenue-share with Circle, and OUSD through a model that makes reserve-sharing the default rather than a negotiated exception.

If Tether were publicly traded, there is a case that it would not trade down on this news at all. USDT's stronghold is emerging markets and offshore dollar liquidity, where users hold and move dollars that the local banking system cannot reliably provide. That gives Tether a different kind of moat: deep liquidity, distribution, and entrenched usage in markets where regulated Western stablecoins are not necessarily the default. OUSD's consortium of Western fintechs, banks and payment companies is built for a different target market. The two are unlikely to compete for the same dollar, at least in the short term.

If Tether were publicly traded, there is a case that it would not trade down on this news at all. USDT's stronghold is emerging markets and offshore dollar liquidity, where users hold and move dollars that the local banking system cannot reliably provide. That gives Tether a different kind of moat: deep liquidity, distribution, and entrenched usage in markets where regulated Western stablecoins are not necessarily the default. OUSD's consortium of Western fintechs, banks and payment companies is built for a different target market. The two are unlikely to compete for the same dollar, at least in the short term.

Tether is also actively buying deeper into its strengths. In July it announced a $20m strategic investment in Brazil's Mercado Bitcoin, backing tokenisation, payments and lending across Latin America, a region where dollar stablecoins are useful for cross-border settlement, dollar savings, payments and access to tokenised financial products. Tether CEO Paolo Ardoino welcomed OUSD with open arms, while also taking a dig at Circle. The subtext, to borrow from Don Draper: Tether doesn't think about USDC at all.

Is this actually bearish for Circle?

Let's rephrase that. Is this news bullish for Circle? Well certainly not. But we know the market can be jittery, and particularly in the face of uncertainty, overreact in both directions.

Directionally, the bearish reaction and surrounding narrative is fair. As noted, OUSD puts direct pressure on the two things that matter most to Circle: its reserve margin and the cost of buying USDC distribution.

On the other hand, OUSD is simply an idea as of now; it is not live, has unknown details and even listed partners like Samsung have disputed participation. And this is where the bull case for Circle actually is. Stablecoins are network businesses, and networks are won on liquidity and integrations. OUSD is trying to match this, but USDC has spent nearly a decade embedding itself across exchanges, DeFi venues, PSPs and now bank custody. That depth is the moat USDC has built. Jeremy Allaire makes the point himself, and he is not wrong: liquidity brings more liquidity, particularly in crypto, and bootstrapping from the ground up, regardless of who you are, is tricky.

There is a second point to this. OUSD is the most heavyweight stablecoin consortium ever assembled: 140+ partners, the card networks, the largest asset manager on earth, Stripe's entire merchant base. If a coalition of that scale cannot break USDC's network effects, the question stops being "who beats Circle" and becomes "what could possibly be bigger than this?" A failed OUSD removes the most credible challenger the market can imagine and, by elimination, strengthens USDC as the default fully regulated offering. If Circle can weather the storm, it may come out stronger: the category leader, and a derisked one. And Tether, sitting in a different market entirely, gets to watch the whole thing play out.

GENIUS already bars issuers from paying yield directly to holders, while the CLARITY debate is circling whether platforms should be able to offer it indirectly. OUSD sidesteps that fight by pushing the economics up a layer: reserve income goes to distribution partners, not end users. With direct yield pretty much off the table, OUSD has chosen to fight on distribution instead.

It is likely the market will continue to treat this situation with uncertainty, and new developments on the OUSD side could change this, whether for better or worse, for Circle. Until OUSD launches, the key things to watch are how USDC supply evolves, whether Circle adjusts its distribution economics, and what levers it can pull to combat what many now frame as an existential threat.