Bitcoin 13F Q1 2026 report

![]() 8 Min. Lesezeit

8 Min. Lesezeit

Professional Bitcoin ownership in the second leg of the bear, Q1 2026

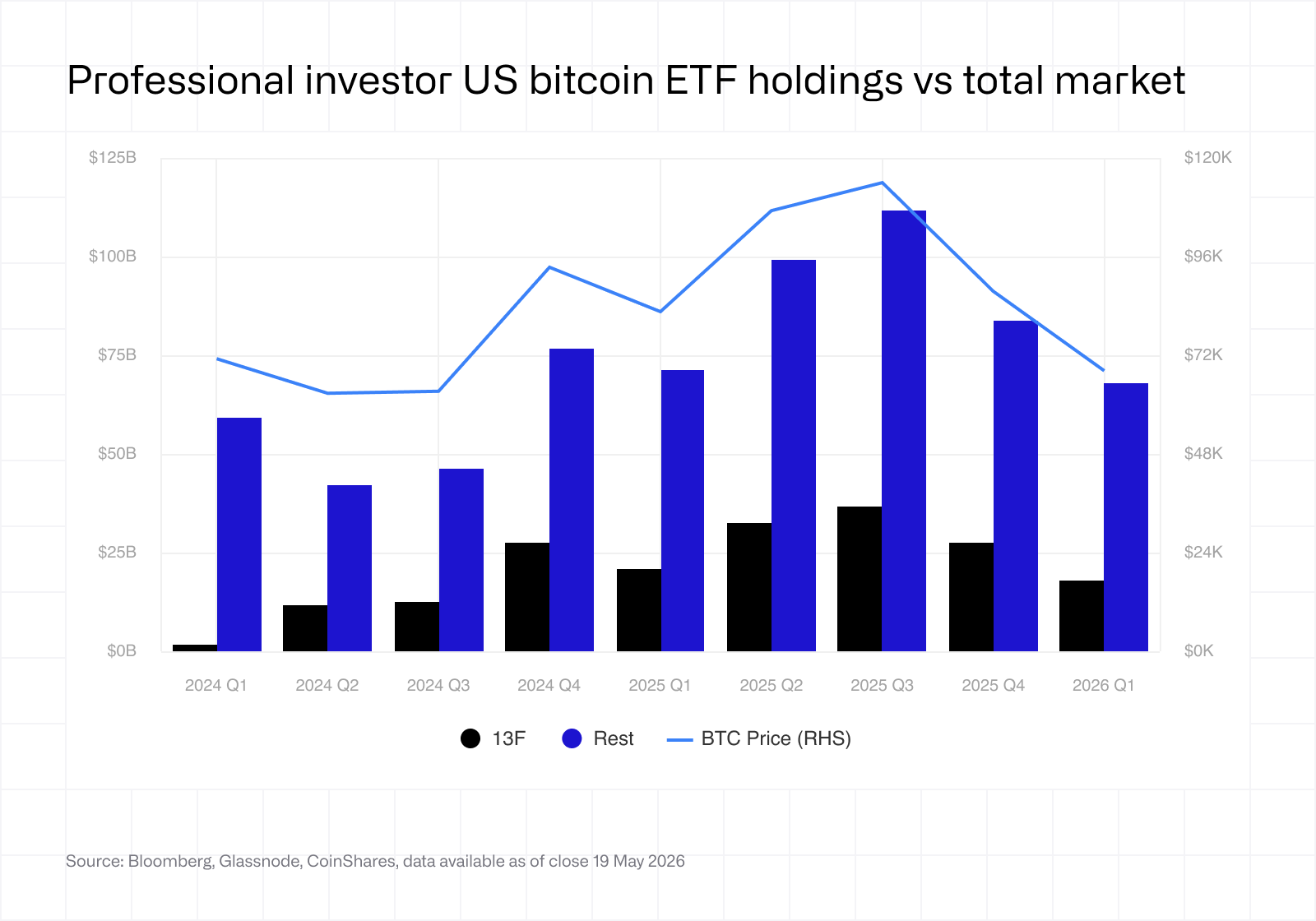

Professional selling deepened materially in Q1, the largest quarterly reduction since the US spot bitcoin ETFs launched. Professional holdings fell in bitcoin equivalent terms from 313k to 261k (-17% QoQ). Total dollar value declined 35% to $17.8B. The 13F share of total US bitcoin ETF AUM reduced from 24.7% to 20.8%.

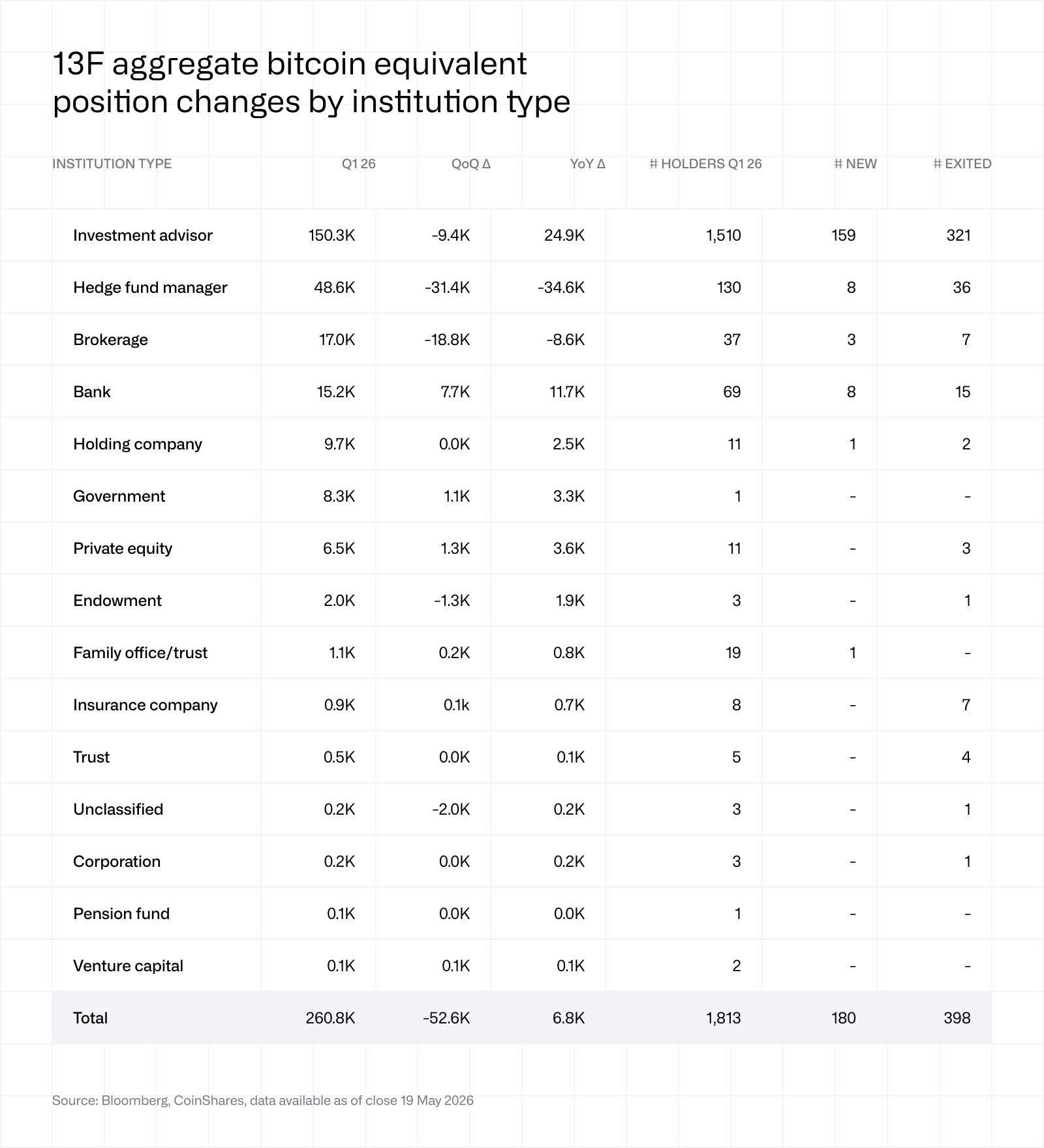

The selling was highly concentrated. Hedge funds (-39% QoQ) and brokerages (-53% QoQ) accounted for 95% of the exposure reduction. Advisors trimmed 6% QoQ, while banks, governments, private equity, family offices, and insurance each added net exposure.

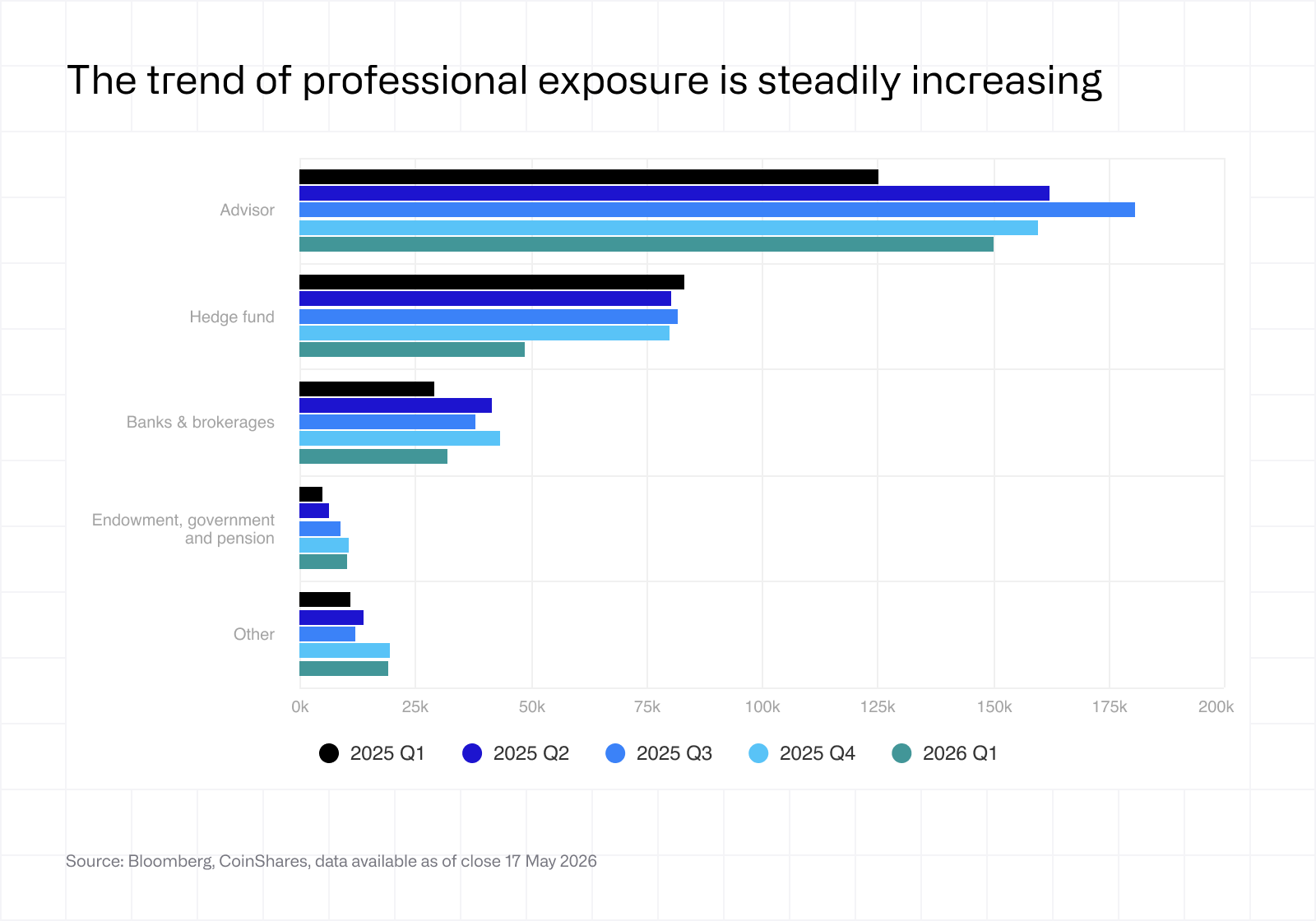

Advisors remain the predominant professional cohort; Banks are a developing investor type; meanwhile, endowments and governments offer compelling storylines. Advisors sit at 150k equiv. BTC holdings, up 20% YoY. Banks at 15.1k BTC, a four times increase YoY. Notably, JPMorgan and Wells Fargo meaningfully grew, and Citigroup filed for the first time.

This dataset is consistent with what bitcoin markets have historically looked like in drawdowns. Leveraged and tactical strategies unwind. Supply redistributes from momentum-driven entrants to long-term holders. What remains, and what perhaps has continued to grow throughout the selloff, is passive, long-duration portfolio allocations; advisors, banks, and sovereigns establishing a long-term strategic holding. That portion of the professional ownership base is the most sustainable, and it largely weathered the storm.

Bitcoin's drawdown deepened in Q1 to an uneasing degree, with the price falling another 22% to roughly $68k by quarter-end but briefly trading below $60k on a single day decline of -14% in early February. That low solidified a roughly 50% drawdown from the October 2025 all-time high above $126k. The price nearly tested its 200-week moving average, one of bitcoin’s longest-standing cyclical support levels. On-chain data registered the largest realized losses since July 2023, the RSI fell to multi-year lows, and sentiment, as measured by the Fear and Greed Index, touched the lowest levels on record.

One of the main questions we had through the first leg of the bear, following the October 2025 high, was whether ETF-era professional ownership would behave reflexively in a deeper drawdown. We found through year-end ownership filings that professionals largely held firm, despite a 23% plunge in price over Q4. But with the Q1 2026 filings now released, and a deeper drawdown complete, the answer to our question can now be fine-tuned.

On the surface, it’s a mixed bag. Parts of the professional investor base meaningfully unwound their positions. Other parts continued to build through the drawdown. The aggregate figures on their own suggest a material exodus, however, the nuances in flow and filing data help clarify, more intricately, that cohorts inclined to trading drove the exodus while those more likely to be investing maintained or accumulated.

Here are your headline reads.

Filers remain net sellers. Bitcoin price falls 22%. ETF AUM falls 23%.

13F filers shed roughly 52.5k BTC in exposure across Q1, taking total professional holdings from 313k to 261k BTC (-17%). The dollar value of the filers fell 35% to $17.8B, with net outflows accounting for roughly $3.6B of the dollar decline and the rest attributable to price.

Beneath the mainly price-driven AUM contraction (111B → 86B, -23%), the composition of ownership meaningfully changed. The 13F filer share fell from 24.7% to 20.8%, the second largest single-quarter reduction in professionals’ ownership share since launching.

The 13F share reduction is worth considering for a moment. In bitcoin terms, 13F holdings are up 2.7% year-over-year, while non-13F holders grew about 16%. That is antithetical to much of the framing of institutional crypto firms, including ourselves at times, as the anticipation has been for professional ownership to outpace the broader bitcoin ETF investor base. More or less, a proclamation of, “The institutions are coming!”.

The 13F share reduction is worth considering for a moment. In bitcoin terms, 13F holdings are up 2.7% year-over-year, while non-13F holders grew about 16%. That is antithetical to much of the framing of institutional crypto firms, including ourselves at times, as the anticipation has been for professional ownership to outpace the broader bitcoin ETF investor base. More or less, a proclamation of, “The institutions are coming!”.

Yet this past quarter, professionals were a meaningful source of market supply, on the margin nudging the price lower.

This market behavior is not new to bitcoin, however. In past price cycles, the same pattern has played out among retail cohorts. Drawdowns flush out holders who came in throughout the prior uptrend's momentum, without establishing a hardened conviction in bitcoin’s long-term investment case. Supply then migrates from those who bought on a whim to those who bought because they have studied it and intend to hold for years.

What is a distinct sign of the times is the participation profile. Professional allocators are almost certainly a greater share of the bitcoin market than cycles past, and newfound growth suggests they are still in the earlier innings of their bitcoin journey. They have likely been aware of it for many years, but only recently have access vehicles like ETFs allowed them to practically or seriously participate. Some of those who entered for the trend are likely simply exiting now that the trend has turned.

Hedge funds and brokerages account for 96% of the selling. Banks and Governments continued to add.

Hedge funds reduced exposure by 31.4k BTC, a -39% QoQ contraction and -42% YoY. Perpetual futures funding rates turned negative on a 30-day average by quarter-end, making the basis trade unprofitable at scale and encouraging unwinds. Add to that a broader leverage flush and tactical opportunities in AI and precious metals competing for capital, and the reductions aren’t so surprising, qualitatively speaking.

Hedge funds reduced exposure by 31.4k BTC, a -39% QoQ contraction and -42% YoY. Perpetual futures funding rates turned negative on a 30-day average by quarter-end, making the basis trade unprofitable at scale and encouraging unwinds. Add to that a broader leverage flush and tactical opportunities in AI and precious metals competing for capital, and the reductions aren’t so surprising, qualitatively speaking.

Brokerages reduced by 18.8k BTC, a 53% QoQ contraction. Two names of which account for most of it. Morgan Stanley fully exited its 8.3k BTC position, which we read as related to the April launch of MSBT, the firm's own bitcoin ETF that does not yet appear in 13F filings. The other is Jane Street, who reduced 10.8k BTC, consistent with what one might expect from a major ETF market maker during a quarter that opened with outflows.

Advisors reduced by 9.4k BTC (-5.9% QoQ), while adding 159 new filers and losing 321 to fully exited positions. At 150.3k BTC, they account for roughly 58% of all 13F bitcoin holdings. Their relative steadiness through Q1 is the single most important datapoint in the filing season, in our opinion, indicative that these holdings likely represent structural, long-term portfolio allocations rather than trade positions.

Banks added 7.8k BTC, more than doubling their size to 15.2k BTC and growing 339% YoY. JPMorgan Chase added 3k BTC, Wells Fargo added 4k BTC, and Intesa Sanpaolo entered with 1.6k BTC. Citigroup also filed for the first time, with a 97 BTC position. At the Strategy World conference, Nisha Surendran, head of digital asset custody development at Citi, indicated the bank planned to launch infrastructure later this year that integrates bitcoin into traditional finance. With JPM, Wells, Bank of America, and Citi all filing, some of the largest US banking franchises are officially on board.

Governments added 1.1k BTC, entirely from the Emirate of Abu Dhabi Mubadala Fund, taking the sovereign cohort to 8.3k BTC. Private equity grew 24% QoQ and 124% YoY. The one contraction outside the tactical cohort was endowments, down 40% QoQ, driven almost entirely by Harvard's 1.3k BTC reduction. Though the Ivy League allocations remain, Harvard still holds 1.7k BTC, Dartmouth at 114 BTC, and Brown at 120 BTC.

Looking ahead

Beyond the price and holdings change activity, regulatory and infrastructural development continued in Q1. The SEC and CFTC classification release, the Department of Labor's proposed 401(k) rule, and the maturation of bitcoin-backed credit instruments advanced during the quarter. Altogether, a sign of encouragement regarding bitcoin’s integration into mainstream financial markets.

Perhaps most notable for the long-term trajectory of bitcoin’s inclusion in modern portfolios, BlackRock published research arguing that elevated stock-bond correlations since 2020 have weakened the traditional 60/40 diversification framework, and that bitcoin and gold can improve outcomes when combined as diversifiers. Their Target Allocation with Alternatives model portfolios already include both. BlackRock's team even coined the title of our now 5 years old research on the topic: "a little bitcoin can go a long way."

It’s refreshing to see the world's largest asset manager agree with our foundational research, and it’s certainly a material development given their wide-spanning distribution.

Since Q1 2026 ended, US spot bitcoin ETF flows have turned positive, totaling roughly +$2.3B through mid-May, after running negative in Q1. Strategy's STRC preferred instrument has also conjured demand, adding approximately $4.1B in the same period, atop the $6.5B accumulated in Q1. Combined ETF and DAT flows for Q2 are near $6.4B through May 17, following a particularly strong April at $6.6B.

Several items bear watching ahead of the Q2 13F filings in mid-August. Morgan Stanley's MSBT, which launched in April, should appear in the data for the first time, likely recovering some of the brokerage position that exited Q1. SpaceX disclosed 18.7k BTC in its S-1 filing, adding another major corporate name to the holder base. A formal update on the US Strategic Bitcoin Reserve is reportedly nearing release, following comments from the Executive Director of the President’s advisory for digital assets, Patrick Witt. The CLARITY Act cleared Senate Banking Committee markup, with prediction markets pricing above 50% odds of 2026 passage, at the time of writing.

On the other hand, external to the crypto industry, the Middle Eastern conflict has persisted into late May. Inflation expectations have increased materially, well above the Federal Reserve's 2% target. Potential rate hikes are now on the table for 2027, and rising bond yields may weigh on risk appetite more broadly.

Q2 filings will show whether the flow improvement since March carried through into professional positioning, if advisors continued to hold and banks continued to build, and whether US ETF investors can continue to weather its first full bear market test. Bitcoin's adoption as a portfolio allocation continues to unfold, and we will continue to monitor its developments.